|

Abstract摘要:

本文运用事件研究方法考虑对股票价格并购公告的效果。该方法引入并在第一部分说明。此外,兼并和收购的定义。市场模式选择估计超额收益。累计异常收益事件窗口期间计算。一个具体的例子是研究,在德国公司的活动。最终的结果显示,还有就是并购与股票价格之间的强关系。而此前有消息称,价格下跌公布的目标公司的股票价格之前,新会增加公布。Event study method is a branch of econometrics to estimate the effect of economic events on the stock price of the company. This paper considers the effect of the mergers and acquisitions announcements on the stock price by using the event study methodology. The method is introduced and explained in the first section. Moreover, the mergers and the acquisitions are defined. The market model is selected to estimate the abnormal returns. Cumulative abnormal returns are calculated during the event window. A concrete case is studywhich are company activities in Germany. The final results show that there is strong relation between the M&As and the stock price. The target company’s stock price will increase before the new is announced while the price declines after the news is published.

1 Introduction介绍

事件研究方法侧重于探讨事件(如兼并,收购,财报公布再融资或行为等)对股票价格(或企业价值)的影响,可以从以下几个方面体现出来的影响效果:平均股价效应,市场收益方差的变化,在存货周转率的变化,在性能业务的变化。事件研究方法是第一个广泛近几十年来应用于金融和经济的文学事件的研究已成为金融和经济文献(FAMAE 1991)的重要组成部分。

事件研究方法可以用来探索事件上的因变量的影响。在这份报告中,股价一家公司进行了研究,以给予投资者更好的投资替代品。在这种情况下该事件被定义为股价超预期事件窗口(黄ShouWoon)中的变化。超额收益反映事件的影响。因此,该事件研究方法试图确定事件如何影响股票价格和在何种程度上该事件是(棕S和J.华纳1980)。Event study methodology focuses on exploring the effect of events (such as mergers, acquisitions, earnings announcement or refinancing behavior, etc.) on the impact of stock price (or enterprise value), the impact can be reflected in the following aspects: the average share price effect, the market income variance changes, changes in the stock turnover, business changes in performance. Event study methodology was first widely used in finance and economic literature on event studies in recent decades has become an important part of the financial and economic literature (FamaE 1991).

The event study methodology can be used to exploring the effect of event on a dependent variable. In this report, the stock price of a company is researched to give investor better investment alternatives. The event in such situation is defined as the change in stock price beyond expectation during the event window(Wong ShouWoon). The abnormal returns reflect the effect of the event. Thus, the event study methodology tries to determine how the event affects the stock price and what extent the event is (Brown S and J. Warner 1980).

2 Literature review文献综述

2.1 Event study method

Event study method actually has a fairly long history. The earliest research can be traced back to the 1930s, Dolly (1933) used the event study methodology to examine the effect of the stock split on the stock price. Subsequently, Myers and Bakay (1948), Barkay (1956, 1957, 1958), Ashley (1962) and other people further improved the development of the event study method, but until 1960s, Ball and Brown published their research, the event study method was able to eventually "mature" (Craig Mackinlay 1997).

2.2 Mergers and acquisitions

Mergers and acquisitions are the modes of independent firms combining together and forming one entity. The connection may be well or hostile with each other. Many researches have explored the M&As. Some of the studies show that they contribute equally while others find each firm dominates corresponding part. Mergers are different from the acquisitions because mergers assume that the two companies are equal sizes or equivalent resources. If one of the companies is much larger than anther, it is viewed as acquisition. Thus, M&As is a corporate strategy, combining the finance as well as the management of the companies with similar function. It can help companies grow quickly in wide area or a new field without creating a new company of child company.

In the economic history, the M&As waves are divided into 5 parts based on the activities in the world. The M&As starts in the late of 19th U.S. there were horizontal mergers in that time. the second wave is between 1916 and 1929, while the main activities are vertical mergers. The third M&As broke out from 1965 to 1969 while the fourth M&As wave took place at 1981 to 1989. Since 1992, the fifth wave, also known as cross-border mergers began. The M&As waves in the history caused great impact on the global economics(Susan Cartwright 2006).

3 Methodology放法论

Generally, the event study consists of s six steps including defining the event as well as event study window, selecting the study sample, choosing a model to measure normal income, estimating the abnormal returns, inspection significant abnormal returns and attaining the empirical results and interpretation (John J. Binder 1998). This part of the paper describes steps and analyzes the corresponding characteristics of the event study methodology.

3.1 Define the event and the event window

Events include mergers and acquisitions, and if researchers concern with the impact of the issuance on shareholder wealth, at this time the event is the additional announcement. Event relates with the estimation window, event windows and afterwards windows, etc. t = 0 is the event date; t = + 1 to T = represents the event window, with a length of ; T = + 1 to T = is estimation window with a length of ; t = +1 to T = is afterwards window, its length is .

The estimation window's role is to estimate the normal income (or estimate normal income model parameters), under normal circumstances, the length of the estimated window should be greater than or equal to 120 days; event window is used to test the stock price whether it reflects the abnormal incident or not. In this paper, an estimated time of 120 days is determined.

3.2 The selection of the study sample

The event study sample selection is very important, whether a company occurring an event should be included in the study sample also need to be carefully considered, especially in small sample studies. For this reason, it should be pre-determined criteria for selection of the sample, such as setting data availability restrictions, trade restrictions, etc.. In this model, a total of 50 German companies over the past two years from 2008 to 2010 are selected as the research sample. All of these companies completed the merger activities.

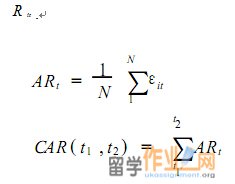

3.3 Normal return calculations

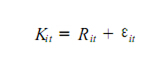

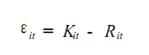

In order to evaluate the impact of the event, it is needed to measure abnormal returns, abnormal return is the difference between securities actual income and normal income during event window period. That is:

is the actual income, is normal income, is abnormal ( or expected ) part. In this decomposition, abnormal return the difference between the actual income and normal income:

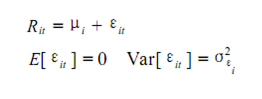

Before definingthe abnormal return, it is necessary to set (or select) normal income.The normal income Kit model includes statistical model and economic model, statistical model is based on asset yield behavior of statistical hypothesis, being not dependent on any economic theory, while economic model is based oninvestorshypothesis, regardless of statistical hypothesis (John J. Binder 1998).

Statistical model is a constant mean value income model. The model is regards the average income of securities as the normal returns during the estimated period (i.e. estimation window ). If is the average income of assert i, then the mean values of earnings model is:

is the income of security I at time t. is the fluctuation item, the variance is .

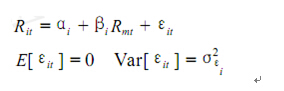

Market model. Market model is a statistical model combining the stock returns and market portfolio income. That is:

represents the income of the securityi at time t while represent the income of market portfolio at time t. is the fluctuation, is variance, and are the parameters.

3.4 Estimating the abnormal returns

After selecting good model for estimating the normal returns, the next step is to estimate the abnormal returns. The equation two shows that the abnormal return is = , is not necessary to estimate, while requires the estimation. Generally, the estimation adopts relevant data in the estimation window. In the event study, market model parameters can be calculated through events which occurred 120 days before data is estimated, and then using the estimated parameters and corresponding data inevent window to calculate the estimated value of .#p#分页标题#e#

3.5 The significant test of abnormal returns

After abnormal returns calculation comes out, the researchers always test the hypotheses of the cumulative average abnormal returns and the extent of the result. The hypothesis test is quite necessary.

During the time before the company publishes the merger or acquisition announcement, some staff may know the inside information and then increasing the share of the company stock so as to get extra income by waiting for the increase of the stock price. When the company announces the news, it is definite that some people can get such income. Thus, the insider information may have positive or negative effect on the company’s activity. The event study method is one of the effective ways to calculate the effect of insider information.

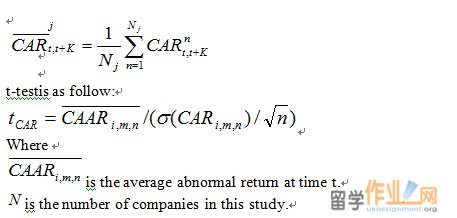

In general, through the test of a certain stock during the events of one day abnormal return, it can infer events during the event period. It needs cumulative abnormal returns during the events of statistical test to determine the overall revenue impact events on the stock. To judge whether there is significant abnormal returns or not, the detection data is used to test the assumption. As the cumulative abnormal return is distributed, the data can construct a n-2 degree freedom of t-distribution. Thus, the formula for calculating the variety is:

t-testis as follow:

Where

is the average abnormal return at time t.

is the number of companies in this study.

3.6 Result and analysis

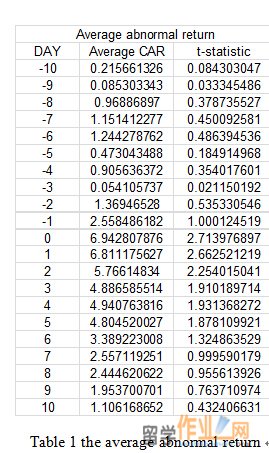

Table 1 the average abnormal return

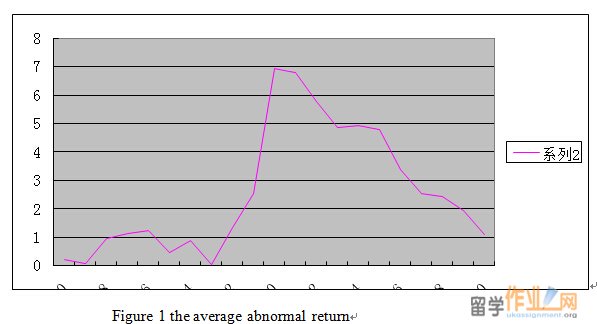

Figure 1 the average abnormal return

The results are showed in the table 1 and figure 1, which reflect the average cumulative abnormal return and the average CAR of the 50 companies in event window [10, 10]. From day -9 to day -6, there is an increase of the cumulative abnormal return, while there is a decrease trend from day -6 to day -3. However, there is a sharp increase between day -3 and day 0.5. And then, the value drops until the value comes to the lowest at day 10. On the day 0, also known as the event day, the cumulative abnormal return is 6.9428 while the t value is 2.72, which indicates the cumulative abnormal return is significant. In the day 10, the value has decreased to 1.10618. According to this research, there is a significant effect of merger announcements on stock returns.

Based on the results, it comes to the conclusion that the event will cast great effect on the stock price. There is a positive effect before the announcement is published while the effect is negative after it is published. Moreover, more details about the model should be discussed. Through the above steps, the empirical results have been obtained. But it is necessary to note that, sometimes, especially with the use of limited event observation data for the study, the empirical results may be greatly influenced by one or two the influence of the company. Therefore, in conclusion or interpretation should be particularly cautious.Based on the above events research steps, we can see there are choices in the event of some steps, such as event window length selection, sample selection, estimation window length selection, with so many choices, it will bring the uncertainty of conclusion of the study and the corresponding explanation. Therefore, in the use of event study, to understand and correctly handle the event study in the presence of ‘variable’ is very necessary.

4 Conclusions总结

The paper uses the event study method to check the influence of the company announcement about the M&As on the stock price. The event study method is provided and discussed on how to apply it in the finance analysis. And then, the M&As is defined and introduced. After all the theories are explained, the paper completes a practical case study on German’s companies. It is presented with specific steps of the event study method and finally comes to the results. The results show that there is strong relation between the M&As and the stock price. The target company’s stock price will increase before the new is announced while the price declines after the news is published. The phenomenon may be result by the insider information. In the last, the event study method is explored and further considerations are pointed out.

LIST OF REFERENCES文献

Fama E 1991, Efficient capital markets, Journal of Finance, Vol. 46, pp.1575-1617

Brown S and J. Warner 1980, Measuring security price performance. Journal of Financial Economics, Vol.8, pp. 205-258

Craig Mackinlay 1997, Event Studies in Economics and Finance, Journal of Economic Literature, Vol. XXXV, pp. 13-39

Susan Cartwright 2006, Thirty Years of Mergers and Acquisitions Research, British Journal of Management, Vol. 17 Issue S1, pp.S1-S5

Kyungmook Lee 1996, MERGERS AND ACQUISITIONS: STRATEGIC - ORGANIZATIONAL FIT AND OUTCOMES, viewed15December 2012http://www. management.wharton.upenn.edu/pennings/documents/mergers_acquisitions.pdf

John J. Binder 1998,The Event Study Methodology Since 1969, Review of Quantitative Finance and Accounting, Vol.11, pp.111–137

|

| 网站地图 |