|

Taps and Plumbing Supplies (TaPS)水龙头和管道用品(水龙头)

The case scenario案例场景

The Taps and Plumbing Supplies (TaPS) business began as a brass and iron foundry, before moving to manufacturing taps. Today, TaPS is one of Auckland’s established supplier of tapware. 水龙头和管道用品(水龙头)业务开始于一个铜和铁铸造厂,然后转向制造水龙头。今天,Taps是奥克兰已建立的Tapware供应商之一。

Taps and Plumbing Supplies (TaPS) manufactures two models of bathroom taps at their Panmure plant. The plant has two production departments - machining and assembly. 水龙头和管道用品(水龙头)在其Panmure工厂生产两种型号的浴室水龙头。工厂有两个生产部门-加工和装配。

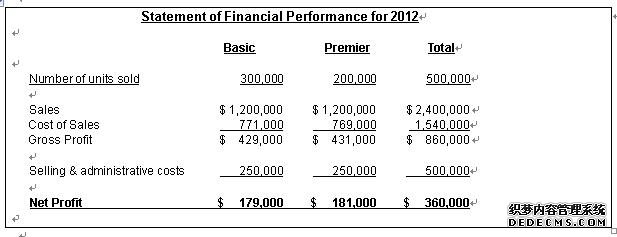

Two models of taps are manufactured - a basic and a premier model. The premier model was introduced in 1998 and it has proved to be both popular and profitable. In 2012 it accounted for 40% of the total units sold and over 50% of the company’s profit. These statistics are shown in the 2012 Statement of Financial Performance. 制造了两种型号的水龙头-一种是基本型,另一种是高级型。卓越模式于1998年推出,并已被证明既受欢迎又有利可图。2012年,该公司的销售额占总销售额的40%,利润占公司利润的50%以上。这些统计数据载于2012年财务业绩表。

The Cost of Sales expense is comprised of direct materials cost ($460,000), direct labour cost ($360,000) and production support costs ($720,000). Of the $720,000 support costs, the management accountant has been able to trace $192,000 directly to the machining department and $168,000 directly to the assembly department. The remaining support costs were attributable to the various service departments. 销售成本包括直接材料成本(460000美元)、直接人工成本(360000美元)和生产支持成本(720000美元)。在72万美元的支持成本中,管理会计可以直接向机械加工部门追溯到19万2千美元,直接向装配部门追溯到16万8千美元。其余的支助费用可归因于各服务部门。

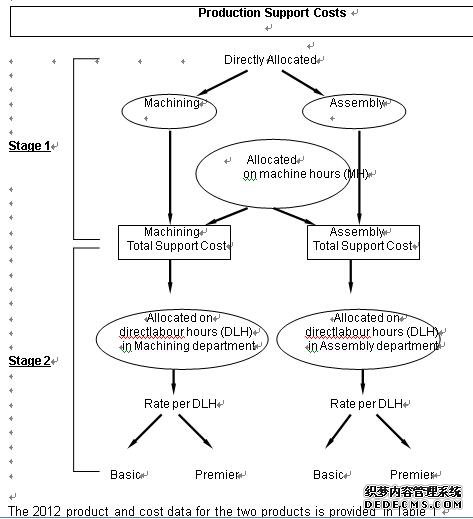

在现有成本分配系统的第一阶段,该服务部门成本(36万美元)根据每个部门使用的机器工时分配给加工和装配部门。

在第2阶段,根据两个生产部门各自的直接工时确定了各自的成本驱动率。这些费率用于将支持成本分配给这两种产品。

In Stage 1 of the existing cost allocation systems this service department cost ($360,000) was allocated to the machining and assembly departments based on the machine hours used in each department.

In Stage 2, separate cost driver rates were determined for the two production departments based on their respective direct labour hours. These rates were used to allocate the support costs to the two products.

Figure 1 illustrates this two stage cost allocation of support costs.

Figure 1 - Two Stage Cost Allocation of Support Costs

TaPS profitability has been declining for the last two years despite the introduction of the Premier model that has now captured over 65% of the share of its segment of the industry. Market share for the Basic model has decreased to 12%. In an attempt to understand the reasons for the decline in profitability, the company has formed a special task force.

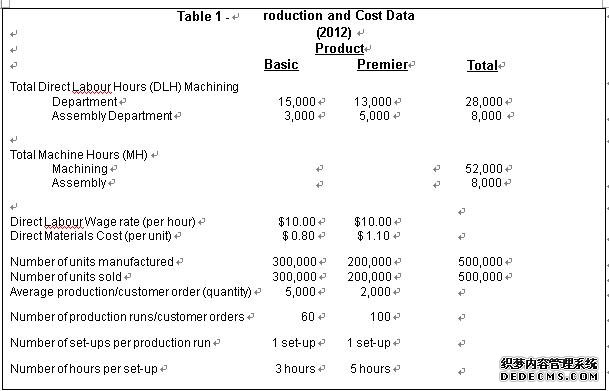

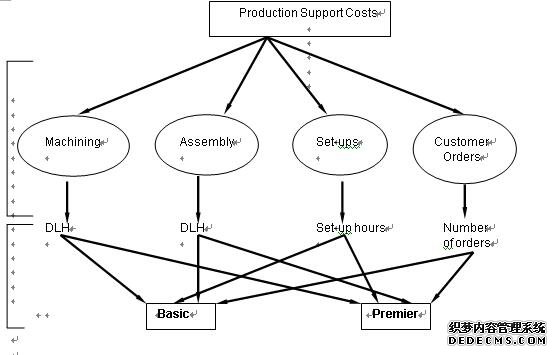

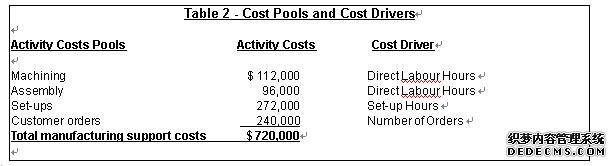

This task force has proposed a new costing system based on an activity analysis that has been undertaken. Three cost drivers have been identified - direct labour hours, set-up hours and number of orders. Production support costs have been traced to four cost pools; each identified with a unique cost driver as presented in Figure 2 and Table 2.

Figure 2 - Two Stage Cost Allocation of Support costs

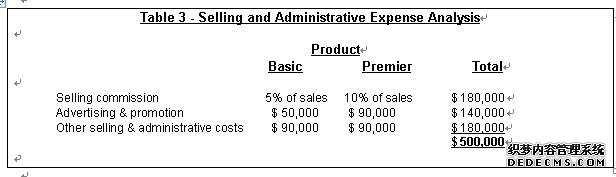

The task force also analysed selling and administrative expenses using an activity analysis. This analysis is given in Table 3.

Question 1 (53 marks)

Required:

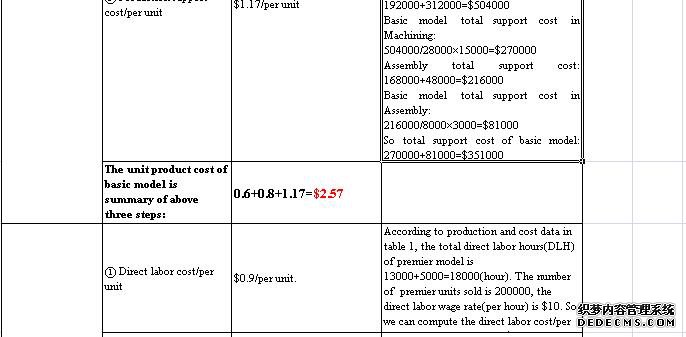

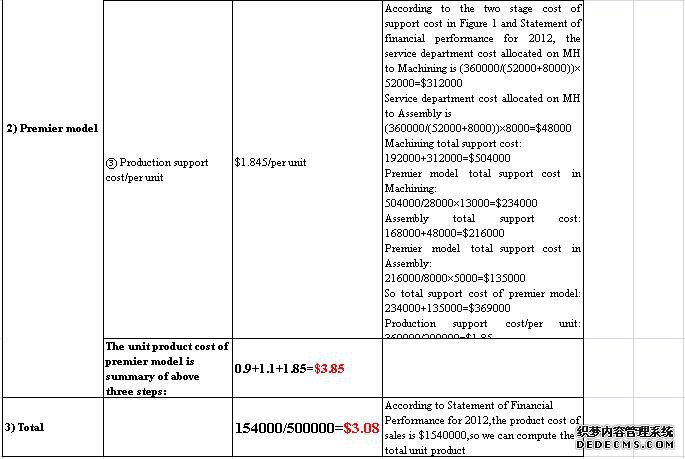

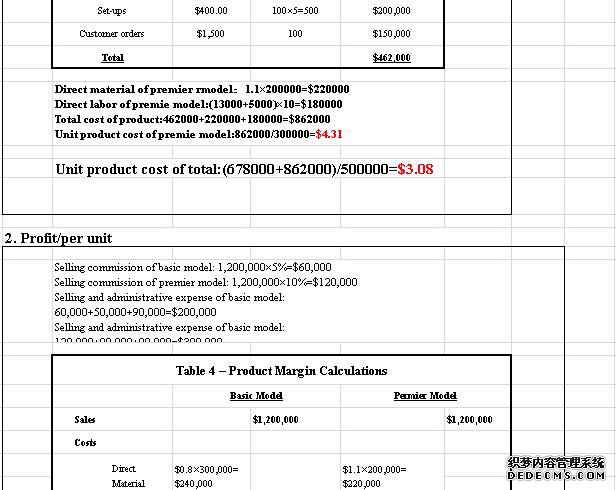

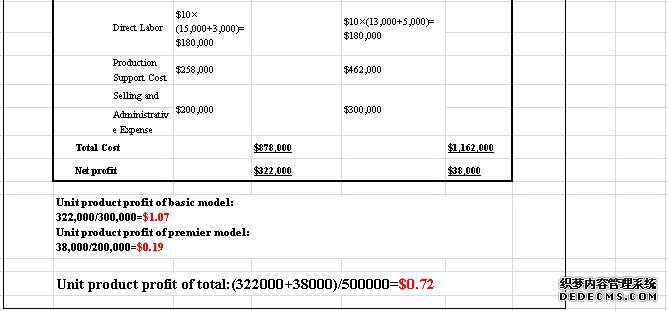

(a) Compute the unit product costs and profit for both the basic and the premier models under the existing costing system.

(Show all the intermediate steps including the cost driver rates and a breakdown of product costs into each of their components)

(15 marks)

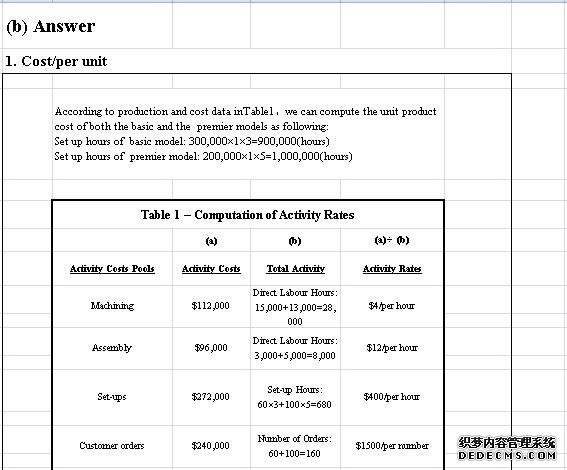

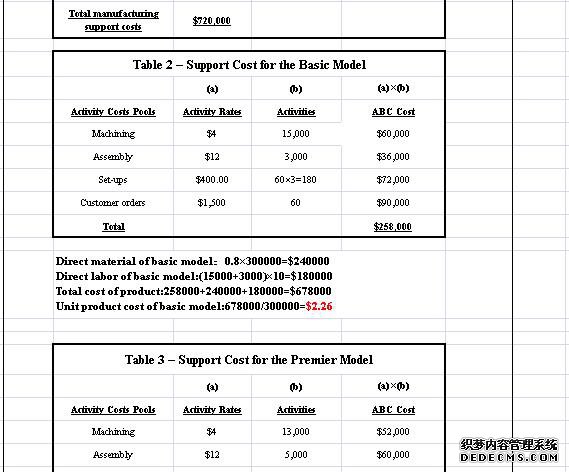

(b) Compute the unit product costs and profit for both the basic and the premier models under the proposed activity-based costing system

(Show all the intermediate steps including the cost driver rates and a breakdown of product costs into each of their components)

(23 marks)

|

| 网站地图 |