|

Sustainability Analysis ReportOf the Adidas Group

Table of contents

1.0 Introduction 3

2.0 Financial Performance Analysis 4

2.1 Gearing and Capital Structures 4

2.2 Profitability Analysis 6

2.3 Asset Efficiency Analysis 8

2.4 Liquidity analysis 9

3.0 Social Performance Analysis 11

4.0 Environmental Performance Analysis 12

5.0 Conclusion 13

Reference List 14

1.0 Introduction引言

阿迪达斯集团是一家体育用品的跨国制造商,总部位于巴伐利亚州的赫佐根纳拉赫(adidas-group.com 2016a)。该公司于1949年由其创始人阿道夫·阿迪达斯(adidas group.com2016a)注册成立。一开始,阿迪达斯是由阿道夫·达斯勒和鲁道夫·达斯勒两兄弟创办的,但后来他们彼此分开了公司。后来,鲁道夫·达斯勒兄弟又创立了另一个体育品牌,名为“普玛”(in.rediff.com 2005)。

阿迪达斯目前在世界体育品牌中排名第二,仅次于耐克(adidas-group.com 2016a)。截至2014年12月31日,公司拥有45917名员工(阿迪达斯集团2014b)。阿迪达斯以“每一位运动员的最佳鞋款”的理念(adidas-group.com 2016b)为支撑,不断改进技术,在设计和功能上取得突破。几项高科技、高品质产品的发明,使公司在奥运会、世界杯等国际体育赛事中屡显辉煌。20世纪60年代末,阿迪达斯在世界鞋业市场排名第一(adidas-group.com 2016a)。然而,20世纪70年代后,由于公众对高质量运动鞋的需求被忽视,阿迪达斯最终被耐克公司取代成为世界顶级品牌(adidas-group.com 2016a)。

阿迪达斯的政策是保持强大的资本基础,以维护投资者、债权人和市场信心,并保持业务的未来发展(阿迪达斯集团2014a),因此,公司制定了财务原则和企业社会责任标准的可持续方式。在社会和环境方面,阿迪达斯采用一系列方法来管理供应链及其自身的生产设施,以提高其治理水平,减少对环境的负面影响(阿迪达斯集团2014b)。

本报告将从财务绩效分析、社会绩效分析和环境绩效分析三个方面对阿迪达斯的可持续性进行深入分析,其中财务绩效分析采用横向和纵向两种方式对公司进行分析。主要数据来源于阿迪达斯2010-2014年度报告披露的财务信息以及其他两个类似体育品牌2014年度报告的相关财务数据。在社会绩效分析和环境绩效分析部分,将对社会责任的重大事件进行阐述和讨论。

The Adidas Groupis a multinational manufacturer of sporting goods and headquarter is located in Herzogenaurach, Bavaria(Adidas-group.com 2016a). The company was registered in 1949 by its founder Adolf AdiDassler(Adidas-group.com2016a).At the very start Adidas was opened by two brothers Adolf Dassler and Rudolf Dassler, but subsequently they parted company with each other.Thenthe brother Rudolf Dassler opened another sports brand, namedpuma (In.rediff.com 2005).

Adidas is currently ranked second in the world’s sporting brand, ranking behind Nike(Adidas-group.com 2016a). As of 31 December 2014, the company had 45,917 employees (Adidas Group 2014b). Supported by the idea of ‘best shoe for each athlete’ (Adidas-group.com 2016b), Adidas keep improving technology and making breakthrough of design and function. Several invention of high-tech and high-quality products make the company shine at the Olympics, World Cup and other international sporting events for many times. In the late 1960s, Adidas ranked first in the world shoes market(Adidas-group.com 2016a). However, after the 1970s, Adidas was eventually replaced by NIKE in the world top spot as a result of the neglect of general public’s demand for high quality sports shoes(Adidas-group.com 2016a).

Adidas’policy is to maintain a strong capital based so as to uphold investor, creditor and market confidence and to sustain future development of the business(Adidas Group 2014a).Therefore the company sets itsfinancial principle as well ascorporate social responsibility standard sustainable way. As for social and environment, Adidas uses a series of approach to managing the supply chain and its own production facilities, so as to improve its governance level and decline the negative impact to the environment(Adidas Group 2014b).

This report will make an in-depth analysis of Adidas’ sustainability from three parts: financial performance analysis, social performance analysis and environmental performance analysis.Wherein, as for financial performance analysis, both horizontal and vertical ways will be used to analyze the company. The major data is from the financial information disclosed in Adidas 2010-2014 annual report, and relevant financial data of other two similar sporting brands’ 2014 annual report. In the parts of social performance analysis and environmental performance analysis, the major events about social responsibility will be illustrated and discussed.

2.0 Financial Performance Analysis

In this section the financial performance is assessed by ratios, whichcan be classified into the following four categories:gearingand capital structures ratios, profitability ratios, asset efficiency ratios andliquidity ratios (Fridson&Alvarez 2011). Detailed analysis will be underway in horizontal and vertical ways. The former means to compare the financial ratios based on Adidas 2010-2014 fiscal year annual report to analyze its development trends, and the latter means to select certain companies in the same industry, for example, here NIKE and puma are selected, and make inter-company comparisons to analyze the strength and location of Adidas among close competitors based on their financial ratios of 2014 fiscal year.

2.1 Gearing and Capital StructuresAnalysis

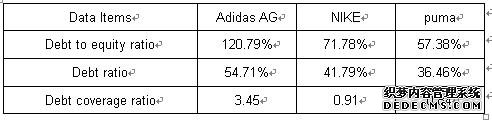

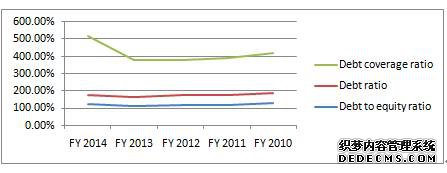

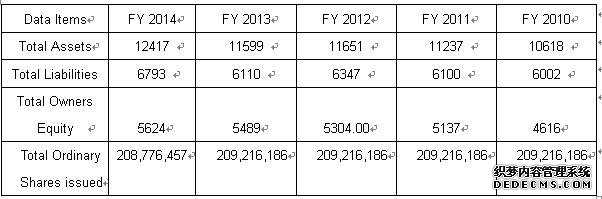

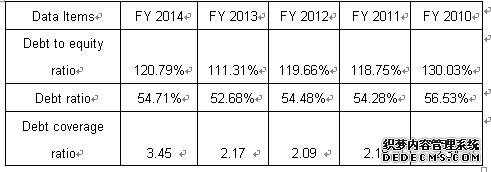

Financial gearing is a measure of a company’s financial leverage, showing the ratio of contribution by the creditors and shareholder during company’s operations (Fridson& Alvarez 2011). Adidas as a sport products company, its equity data from FY 2010 to 2014 is showed as table 1. And the relevant data of NIKE and puma is also obtainable, andthen debt to equity ratio, debt ratio and debt coverage ratio could be calculated. They are listed and showed as table 2, table 3 and graph 1.

Table 1: The capital data of the Adidas AG from FY 2010 to 2014(€ in millions)(Adidas Group 2010 2011 2012 2013 2014)

Graph 1: The Capital structures and gearing ratios of the Adidas AG from FY 2010 to 2014

According to the tables and the graph, on the one hand, in horizontal, in addition to the significantly increase of debt coverage ratios in 2014, Adidas has a very stable state in Capital structures and gearing ratios. From the disclosures in Adidas 2014 annual report, the company issued two bonds with an overall volume of € 1 billion, at the meanwhile there was a share buyback program with a volume of € 300 million in 2014 (Adidas Group 2014a). These are the very reasons of the significantly increase of debt coverage ratios in 2014. On the other hand, in vertical, the three ratios of Adidas all greater than other two companies, which indicate that compared with NIKE and puma, Adidas has a riskier financing structure and weaker long-term solvency ability. But on the other side, the value of Adidas’ debt ratio and debt to equity ratio is stable and in normal range. Taking Adidas’ plan to seek to maintain a balance between a higher return on equity with higher levels of borrowings and security into account (Adidas Group 2014a), Adidas’ issuance of bonds in 2014 are reasonable and it is apparent that the company is trying to control and utilize its financial leverage better.

2.2 Profitability Analysis

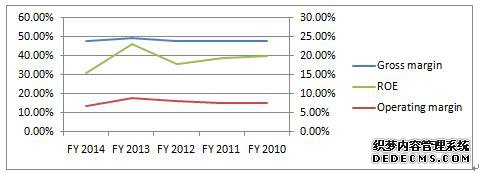

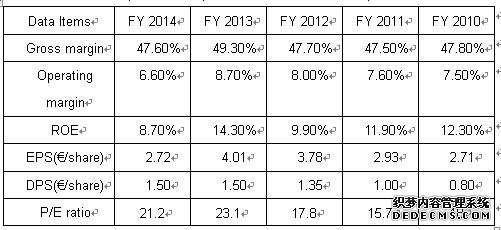

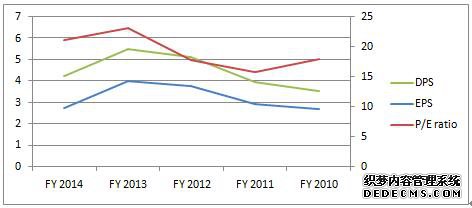

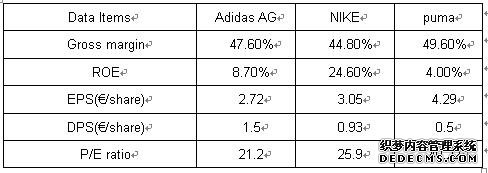

Profitability is corporate’s ability to access profits, which is an important indicator for the investors to judge the financial performance of the company (Fridson& Alvarez 2011). There are several ratios can measure the profitability and in this part gross margin, operating margin, ROE, EPS, DPS and P/E ratio are selected. Relevant data from annual report are listed and showed as table 4, table 5 and graph 2, graph 3.#p#分页标题#e#

Table 4: The Profitability ratios of the Adidas AG from FY 2010 to 2014

These ratios can be classified into two groups. One is common companies’ ratio, including gross margin, operating margin and ROE; the other is listed companies’ ratio, DPS, EPS and P/E ratio included. As for common ratios, in horizontal, the three ratios in 2014 are decreased compared with 2013, and before 2013 the trend is basically positive. And the changes are precisely reflected on equity market. The DPS, EPS, P/E ratio in 2014 are all decreased compared with 2013. According to the annual report, the decrease of operating profit caused the decline of profitability ratios, and it comes from two big parts: the negative impact of Russia economic downturn and the misjudgment of golf business market (Adidas Group2014a).

Graph 2: The Profitability ratios of the Adidas AG from FY 2010 to 2014

Graph 3: The Market performance data of the Adidas AG from FY 2010 to 2014

In vertical, affected by the operating profit decline, Adidas’ ratios are at a disadvantage compared with NIKE and puma. However, in terms of DPS, Adidas is greater much more than other two companies, which indicate that Adidas focus on shareholders’ benefit a lot. From Adidas’ 2014 annual report, the company will continue the buyback, so the equity market performance tends to rebound( Adidas Group 2014a).

Table 5: The Profitability ratios of the Adidas AG, NIKE and puma in FY 2014

2.3 Asset Efficiency Analysis

The asset efficiency means that company’s ability of asset management, which can be weighed by asset turnover ratio, days inventory ratio and days debtors ratio. The asset efficiency reflects company’s cash cycle and activity cycle (Fridson& Alvarez 2011). The relevant data are listed in table 6, table 7and showed as graph 4.

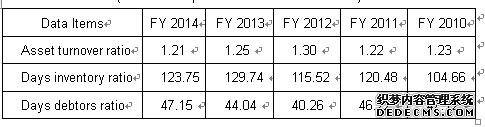

Table 6: The Asset efficiency ratios of the Adidas AG from FY 2010 to 2014

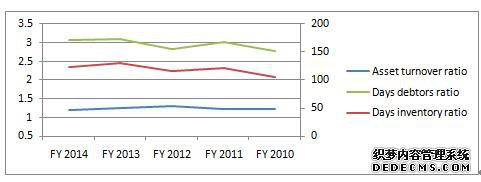

Graph 4: The Asset efficiency ratios of the Adidas AG from FY 2010 to 2014

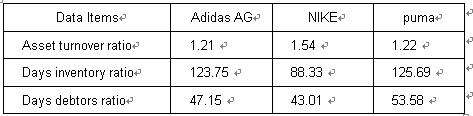

In horizontal, the value of Adidas asset efficiency ratios tends to be steady and only has slight undulate. In vertical, as can be seen, Adidas’ asset efficiency is lower than NIKE but higher than puma, namely at the middle level. From data table, in 2014, the asset turnover ratio of Adidas is 1.21 and the days inventory ratio is 123.75, which means that Adidas sell out its inventory 1.21 times and spend 123.75 days in per time of inventories turnover on average. At the meanwhile, the days debtors ratio in 2014 is 47.15, meaning that it cost Adidas 47.5 days to recover the account receivables on average. In fact, why long-term negative global golf market brought huge pressure to Adidas and caused the decline of profitability in 2014 is directly related to the high level of inventory (Adidas Group 2014a). Therefore, Adidas need to improve its inventory management.

Table 7: The Asset efficiency ratios of the Adidas AG, NIKE and puma in FY 2014

(Adidas Group 2014) (NIKE 2014) (Puma 2014)

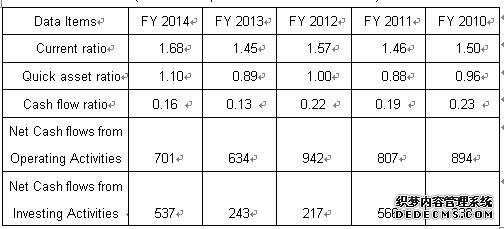

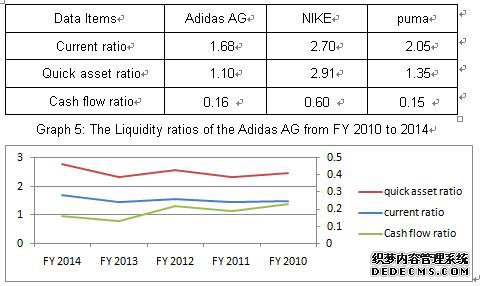

2.4 Liquidity analysis

Liquidity is the company's ability to generate cash and stands for the volume of assets which can be turned into cash in the near future. Liquidity determines the short-term solvency ability of company (Fridson& Alvarez 2011). Liquidity ratios include current ratio, quick asset ratio and cash flow ratio. Relevant Liquidity data is listed in table 8, table 9 and showed as graph 5.

Table 8: The Liquidity ratios of the Adidas AG from FY 2010 to 2014

(Adidas Group 2010 2011 2012 2013 2014)

Graph 5: The Liquidity ratios of the Adidas AG from FY 2010 to 2014

According to graph 9, the current ratio and the quick asset ratio from 2010 to 2014 tend to rise. However, the cash flow ratio tends to decline. According to graph 10, Adidas’ liquidity level is similar to puma and lower than NIKE. That shows Adidas has worse financial flexibility than NIKE. However, other than cash flow ratio of Adidas is too low, the value of the other two ratios are both at a normal level, therefore, it will not have a great risk.

3.0 Social Performance Analysis

As common public are more and more concentrate on company governance ethics, shareholder theory is gradually replaced by stakeholder theory. In this trend, companies will not disregard the social responsibility so long as they want sustainable development. Conversely, as for corporate social responsibility, those companies who performance well are worth to invest. As of 2014, Adidas has issued sustainable report for 15 years, which indicate Adidas’ attitude to CSR is active (Adidas Group 2014b). The analysis of Adidas’ social performance includes three parts: supply chain management, human resource management and contributions to the community.

As the second-largest sporting goods manufacturer in the world, Adidas’ supply chain is complex. Then during the overall producing process, there are many aspects need to be managed and controlled. Above all, as Adidas claimed, itssuppliers will be assessed against many of critical compliance issuesbefore cooperate(Adidas Group 2014b). Then, several measures are taken to control thequality of suppliers’ factories, such as audits, training sessions and warning letters, etc(Adidas Group 2014b). As for human resource, in 2014, the global employee base of the Adidas Group has increased further(Adidas Group 2014b). The company maintained a focus on the sex ratio and the health as well as safety of employees(Adidas Group 2014b).In 2014, Adidas to make donations for the respective requests, the amount decreased compared to 2013 while the project increased(Adidas Group 2014b). Adidas focus on the urgent need for donor groups, such as the Turkish-Syrian border(Adidas Group 2014b). In addition, the company makes employee involved in the donations much more.

However, there are some critical voices from the world andAdidas has been criticized for operating sweatshops (Ekklesia 2012).Back in 2005, Adidas was exposed that 33 workers at the Panarub factory in Java were fired after striking for higher wages (Oxfam Australia 2006). At the meanwhile, it is said that Adidas’ suppliers approved standard does notimplemented in practice(Oxfam Australia 2006). What’s more, in 2012, an organization called War on Want substituted Adidas’ price tag in London stores for 34p ones, which related to the hourly wage Adidas paid for the Indonesian workers (War on Want 2012). According to this series of events, Adidas seems to be contrary to the suppliers’ approved standards just for getting cheap labor, which is not consistent with the code of ethics and violates thedeontological theories obviously.

4.0 Environmental Performance Analysis

In terms of environmental responsibility, Adidas hasresponded positively to the initiative of ‘Green Company’for years (Adidas Group 2014b). The company makes many corporate sites certified according to international environmental management standard ISO 14001 standard (Adidas Group 2014b). According to Adidas’ business character, the performance can be assorted into two parts: productive process and freight.

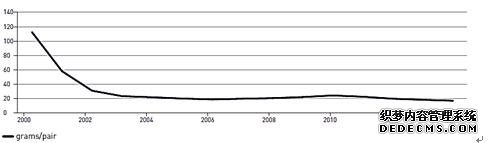

For productive process, other thanAdidas’ strict supervision to suppliers' factories, the company controls its several indexes strictly to makes its performance greater during its operation, such as carbon emissions and the consumptions of water, energy as well as paper. In addition, suppliers will be asked to decrease the use of Volatile Organic Compounds to protect consumers’ health as well as the environment (Adidas Group 2014b). From 2000 to 2014 the reduction, as showed in graph 6, is notable.For freight, Adidas keeps tracking their transporting mode’s impact to environment and tries to optimize the mode to reduce the negative impact (Adidas Group 2014b).

Graph 6: Reduction of VOC exposure in grams/pair of athletic sport shoes (Adidas Group 2014b)

In 2011, Adidas cancelled the contract with Asia pulp & paper, which was Adidas’ long-term wrapper cooperator for many years but considered to be a “forest criminal” since it destroyed “precious habitat” in Indonesia‘s rainforest(Radford 2011),. For this sake, Adidas required commendation from Phil Radford, Director of Greenpeace Executive (Mother Jones 2013). This decision, actually, is consistent with the Ethical utilitarianism.#p#分页标题#e#

5.0 Conclusion

As analyzed above, Adidas has stable long-term financial structure, so its long-term solvency is great; Adidas has low but normal liquidity ratios, so its short-term solvency is above the normal level; Adidas has great profitability ratios and the company concentrate on the shareholders’ warfare, so the company has great ability to access profits; Adidas has relatively lower asset efficiency ratio, so its ability of asset like inventory and account receivables needs to improve. Therefore, the overall financial performance is great. Together with its policy of maintain a balance between a higher return on equity with higher levels of liability(Adidas Group 2014a), Adidas’ capital structure will be optimized in the future, and further the financial performance will be better. On the other hand, the social and environmental performance is generally good. Even there was scandal news about Adidas, its major contributions to social and environment could not be ignored. Further, it is reasonable to believe Adidas is on the way to better cooperate social and environmental performance. To sum up, the Adidas Group is a companyworthyof investment. The company has not only maturity of long-term corporate governance but also growth out of structure innovation.

Reference List

Adidas Group. (2010) Fit for the Future- Adidas Annual Report 2010.Retrieved September 14, 2016

Adidas Group. (2011) Together We Win - Adidas Annual Report 2011.Retrieved September 14, 2016

Adidas Group. (2012) Pushing Boundaries - Adidas Annual Report 2012.Retrieved September 14, 2016

Adidas Group. (2013)For the Love of Sport - Adidas Annual Report 2013.Retrieved September 14, 2016

Adidas Group. (2014a) Make a Difference - Adidas Annual Report 2014. Retrieved September 14, 2016

Adidas Group. (2014b) Make a Difference - SUSTAINABILITY PROGRESS REPORT 2014, Retrieved September 14, 2016

Adidas-group.com 2016a, Adidas Group History, Retrieved September 14, 2016

Adidas-group.com 2016b, Adidas Group Profile, Retrieved September 14, 2016

Ekklesia 2012, Adidas criticised for 'sweatshop' Olympic merchandise, Retrieved September 14, 2016

Fridson, MS, & Alvarez, F 2011, Wiley Finance : Financial Statement Analysis Workbook : A Practitioner's Guide (4), Wiley, Hoboken, US. Available from: ProQuestebrary.

In.rediff.com 2005, How Adidas and Puma were born? , Retrieved September 14, 2016

Mother Jones 2013, Paper Giant Pledges to Leave the Poor Rainforest Alone. Finally. , Retrieved September 14, 2016

NIKE, INC. (2014) Annual Report on Form 10-K. Retrieved September 14, 2016

Oxfam Australia 2006, Inside Adidas' Indonesian Factories, Retrieved September 14, 2016

Puma.(2014) Forever Faster- Annual Report 2014.Retrieved September 14, 2016.

Radford, P 2011, Hasbro Turns Over a New Leaf, Steps Up For Rainforests, Huffington Post. Retrieved September 14, 2016.

War on Want 2012,Trying out our Adidas Clothing Tags in the Sportswear Section of a Big London Department Store, Retrieved September 14, 2016

|

| 网站地图 |