|

The case scenario情况 Taps and Plumbing Supplies (TaPS) manufactures two models of bathroom taps at their Panmure plant. The plant has two production departments - machining and assembly.水龙头和水暖器材(TAPS)生产两种型号的浴室水龙头在他们潘默尔厂房。该厂有两个生产部门 - 机械加工和装配

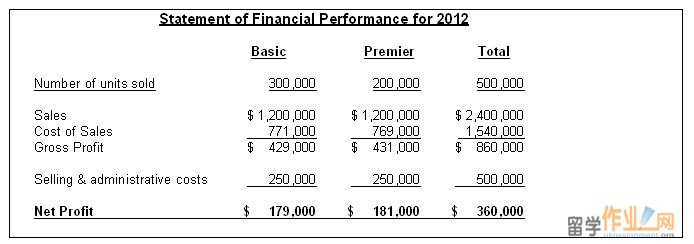

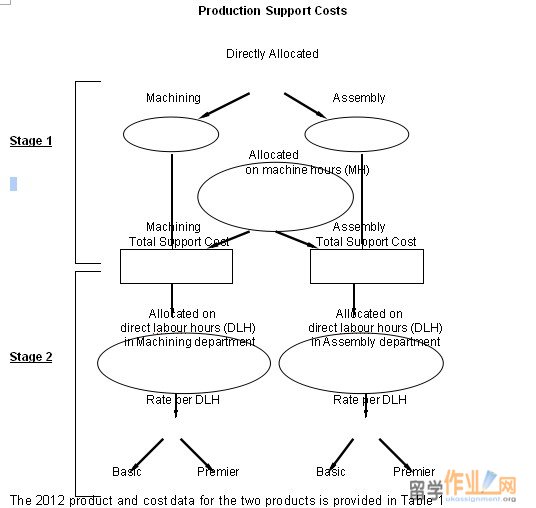

The Cost of Sales expense is comprised of direct materials cost ($460,000), direct labour cost ($360,000) and production support costs ($720,000). Of the $720,000 support costs, the management accountant has been able to trace $192,000 directly to the machining department and $168,000 directly to the assembly department. The remaining support costs were attributable to the various service departments.销售费用的成本包括直接材料成本($460,000),直接劳工成本($360,000)和生产支持成本($720,000)。 $720,000的支持成本,管理会计已经能够跟踪$192,000直接到加工部门和168000美元直接装配部。余下的支持成本占各种服务部门。 In Stage 1 of the existing cost allocation systems this service department cost ($360,000) was allocated to the machining and assembly departments based on the machine hours used in each department. In Stage 2, separate cost driver rates were determined for the two production departments based on their respective direct labour hours. These rates were used to allocate the support costs to the two products. Figure 1 illustrates this two stage cost allocation of support costs.

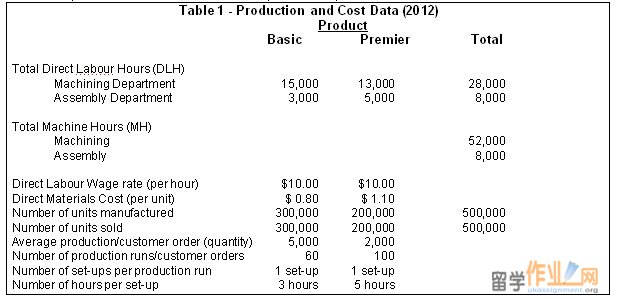

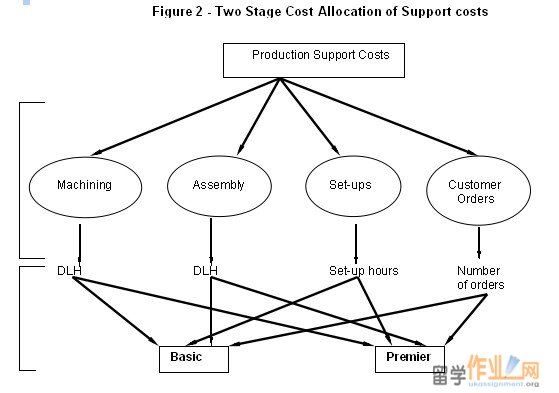

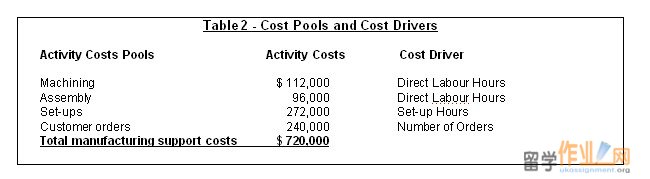

This task force has proposed a new costing system based on an activity analysis that has been undertaken. Three cost drivers have been identified - direct labour hours, set-up hours and number of orders. Production support costs have been traced to four cost pools; each identified with a unique cost driver as presented in Figure 2 and Table 2.

(b) Compute the unit product costs and profit for both the basic and the premier models under the proposed activity-based costing system (c) Explain why the cost and profitability estimates for each product differ under the two costs systems and discuss why these differences might be important to the company. (15 marks)

|

| 网站地图 |

TaPS profitability has been declining for the last two years despite the introduction of the Premier model that has now captured over 65% of the share of its segment of the industry. Market share for the Basic model has decreased to 12%. In an attempt to understand the reasons for the decline in profitability, the company has formed a special task force.

TaPS profitability has been declining for the last two years despite the introduction of the Premier model that has now captured over 65% of the share of its segment of the industry. Market share for the Basic model has decreased to 12%. In an attempt to understand the reasons for the decline in profitability, the company has formed a special task force.

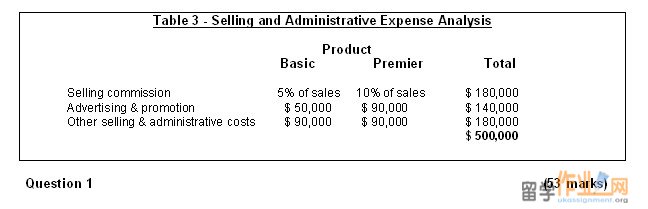

The task force also analysed selling and administrative expenses using an activity analysis. This analysis is given in Table 3.

The task force also analysed selling and administrative expenses using an activity analysis. This analysis is given in Table 3. Required:

Required: