|

导读:本文是一篇新西兰作业范文,本报告旨在从2005年8月至2012年6月,运用法玛-法国三因子月收益模型,对五家公司的股票进行实证研究,包括埃克森美孚公司(XOM)、谷歌公司(Google)、波音公司(Boeing)、纳什芬奇食品分销公司(Nash Finch Food Distribution Company)和立陶宛汽车公司(Lithia Motors Company)。共83次观察。并对回归结果作了简单的解释。其次,用同一模型进行了两个次周期的回归,第一个周期为2005年8月至2008年7月,第二个周期为2008年8月至2012年6月。它将说明这两个子周期之间的区别。最后,本报告将对哪家公司的股权证券值得投资提出建议。

This report aims to make an empirical study about five companies’ equity securities, which include Exxon Mobil Company (XOM), Google Company (GOOG), Boeing Company (BA), Nash Finch food Distribution Company (NAFC) and Lithia Motors Company (LAD), using the Fama-French three factor model with monthly return, starting from August 2005 to June 2012, 83 observations in total. And it also makes a simple explanation about the regression results. Next, it enters into a two sub-periods’ regression with the same model, with period one from August 2005 to July 2008 and period two from August 2008 to June 2012. And it will illustrate the difference between the two sub-periods. Lastly, this report will make a suggestion about which company’s equity security is worth investing.

鉴于资本资产定价模型在某些限制性假设下是成立的,导致资本资产定价模型的实证研究结果不符合研究者的要求,FAMA和French开发了一个三因素资产定价模型来改善其不良绩效。除市场风险因素外,三因素模型还考虑了规模因素和账面市值因素,增加的两个因素与股票收益率显著相关(Clive,2004年)。

Given that the capital asset pricing model holds water under some restrictive assumptions which leads to the empirical study results from capital asset pricing model does not satisfy the researchers, Fama and French developed a three factor asset pricing model to improve its poor performance. In addition to the market risk factor, the three factor model takes size factor and book to market value factor into consideration, the added two factors turns out to be significantly correlated to the stock returns (Clive, 2004).

Fama-French三因素定价模型于1993年提出,具体描述如下:

The Fama French three factor pricing model was proposed in 1993, which is described as follows:

表示超额市场收益;smb表示小公司对大公司的差异收益,也称为规模系数;hml表示高帐面对市场比率与低帐面对市场比率的差异收益,也称为价值系数。系数,,分别是三个因素中每一个的权益的betas,即因子负荷。回归残差的标准差表示特殊风险。与资本资产定价模型相比,该模型包括上述三个系统风险因素(Bodie、Kane和Marcus,2012年)。Fama和French发现,规模与股票回报率之间存在负相关,而账面市值对平均股票回报率更为积极(Fama、French和Kenneth,1993)。

And indicates the excess market return; SMB means the differential return on small firms versus large firms, which is also called the size factor; HML means the differential returns on high book to market ratios versus those firms with low book to market ratio, which is also named value factor. The coefficients of,, are respectively the betas of the equity on each of the three factors, i.e. factor loadings. And the standard deviation of the regression residual denotes the idiosyncratic risk. In contrast to capital asset pricing model, this model includes three systematic risk factors as mentioned above (Bodie, Kane and Marcus, 2012).

Fama and French find out that there is a negative relation between size and stock return, while the book to market value is stronger positive to the average stock return (Fama, French and Kenneth, 1993).

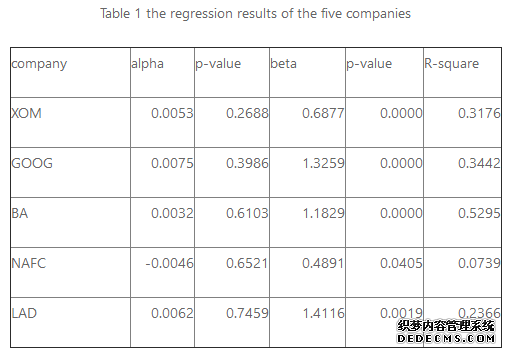

整个期间的回归结果如表1所示。alpha、beta、size和value分别是截距系数、市场超额收益系数、smb和hml的系数。iv是特殊波动率的缩写,根据fama-french在1993年的研究结果(chen和petkov),本报告使用残值的标准差作为特殊波动率。A.2012年,法玛、法兰西和肯尼思,1993年)。

The whole period regression results are presented in table 1 as follows. Alpha, beta, size and value are respectively the coefficients of the intercept, market excess return, SMB and HML.IV is short for the idiosyncratic volatility, and this report uses the standard deviation of the residual value to act as the idiosyncratic volatility, which is according to the research results of Fama- French in 1993 (Chen and Petkova. 2012, Fama, French and Kenneth, 1993).

从表中可以明显看出,5只股票的截距都非常接近于零,同时,在95%的置信水平下,每个系数的p值都大于5%。结果表明,各回归方程的截距与零无关。无明显证据表明,任何股票安全性都优于三因素模型。

It obviously can be seen from the table, the intercepts of the five stocks are all very close to zero, at the same time, the p value of each coefficient are all greater than 5 percent at the confidence level of 95 percent. The results indicate that the intercept of each regression equation is indifferent to zero. Then no significant evidence shows that any equity secuity outperform the three factor model.

贝塔指数显示,只有XOM和NAFC是防御性股票,其他三家是积极性股票;也就是说,goog、ba和lad公司的系统风险高于市场风险。同时,五个β系数的p值都小于5%,这意味着回归结果与0有显著差异。

The betas showed that only XOM and NAFC are defensive stocks, the other three are aggressive stocks; that is to say, the systematic risks of GOOG、BA and LAD companies are higher than the market risk. At the same time, the p values of the five beta coefficients are all less than 5 percent, which means the regression results are significant different from zero.

因子负荷在某种程度上与公司基本面一致,表2所示的结果可以支持这一点。先前的文献表明,小型资本化股票的投资回报率相对较高,账面价值较高的公司往往获得较高的回报率(Nguyen&Tran,2012年)。表2显示,XOM、GOOG、BA的规模远大于NAFC和LAD,前三家公司的系数为负,后两家公司的系数为正,与前面的结果一致。除BA公司外,其他四家公司,NAFC、LAD、XOM和GOOG,账面市值越高,系数越高。总的来说,因素负荷在很大程度上符合公司的基本原则。

The factor loadings are consistent with the company fundamentals to some degree, which can be supported by the results showed in table 2. The previous literature revealed that the small capitalization stocks would have relatively higher investment return and higher book-to-market value company tended to earn a high rate of return (Nguyen & Tran, 2012). Table 2 shows that the size of XOM, GOOG, BA are much larger than NAFC and LAD, meanwhile, the coefficient of the first three companies are negative and the latter two are positive, which is in accordance with the previous results. Apart from company BA, the other four companies, NAFC, LAD, XOM and GOOG, the higher book-to-market value, the higher coefficient. As a whole, the factor loadings are at largely fit in with the company fundamentals.

Grounded on the regression results, the Fama-French three factor model is an appropriate model to price the five companies’ stocks to a certain degree. First of all, the p-values of alpha are not significant, which means that the hypothesis of the intercept being zero can be accepted. And most of the R-squares exceed 30 percent. And a large part of the size coefficients are significant, that is to say the size factor can explain the stock return, though the value coefficient is not that statistically significant.

|

| 网站地图 |