|

ABF305 Investment Management

Lecture 6

ABF305投资管理

第6讲

Overview of today’s lecture

今天的讲座概述

Use of the Payoff and Profit diagram.

回报及利润图使用。

Option trading strategies.

期权交易策略。

Put-Call parity theorem.

认沽呼叫平价定理。

Two-state option pricing.

两状态期权定价。

An option is a derivative:

Derivatives are instruments whose market value ultimately depends upon, or derives its value from the value of a more fundamental investment vehicle called the underlying asset or security.

Options can be used for hedging or speculation:

选项可用于对冲或投机:

Hedging ‘is a trading strategy in which derivative securities are used to replace or completely offset a counter-party’s risk exposure to an underlying asset’. (Reilly and Brown, ‘Investment Analysis and Portfolio Management’ 8th Edition).

对冲“是一种衍生证券的交易策略被用来取代或完全抵消一个对手方的风险相关资产。 (Reilly和布朗,“投资分析与组合管理”第8版)。

‘Hedging is investing in an asset to reduce the overall risk of a portfolio’ (Bodie, Kane and Marcus, ‘Investments’ 8th Edition).

“对冲投资资产,以降低整体投资组合的风险(博迪,凯恩和马库斯,”投资“第八版)。

Option trading strategies.

期权交易策略。

Protective Put. 保护性卖权。

Covered Call. 备兑认购。

Straddle. 跨越。

Spread. 蔓延。

Collar. 衣领。

Protective Put

A protective put is when you have a position in an underlying stock and you buy a put to protect against a drop in the stock’s price. *

The official definition of a protective put is: The purchase of stock combined with a put option that guarantees minimum proceeds equal to the put’s exercise price (Bodie, Kane and Marcus, ‘Investments’ 8th Edition).

Protective Put payoff and profit diagram.

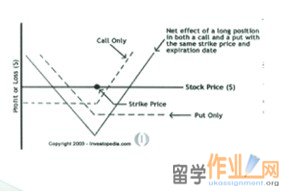

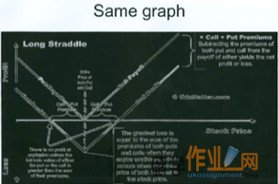

A Straddle

A long straddle is established by buying both a call and a put option on a stock, each with the same exercise price and expiration date. The straddle is a useful option strategy when your viewpoint is that a stock price will move a lot in price but you are not sure in which direction it will move. The worst case scenario for a straddle is no movement in the stock price.

The textbook definition of a straddle is ‘ a combination of buying both a call and a put on the same asset, each with the same exercise price and expiration date. The purpose is to profit from expected volatility’, (Bodie, Kane and Marcus ‘Investments’ 8th Edition).

Straddle variations:

Strips and straps are variations of straddles.

A strip is two puts and one call on a security with the same exercise price and maturity while a strap is two calls and one put. The purpose of creating strips and straps is that they bet on a direction of the volatility of the stock price.

A ‘spread’, and a ‘collar’.

A spread is combination of two or more call options (or two or more puts) on the same stock with differing exercise prices or time to maturity. Some are bought, while others are sold or written.

A collar is an option strategy which brackets the value of a portfolio between two bounds. It does so, for example, by a protective put to place a lower boundary and writing a call to place an upper bound.

The put-call parity theorem relates the prices of put and call options as follows:

Where P is the put price, C is the call price, S0 is the stock price, X is the exercise price of both the call and the put options. PV(X) is the present value of a claim to X dollars to be paid at the expiration date of the options, and PV(dividends) is the present value of dividends to be paid before option expiration.

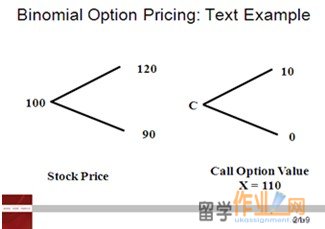

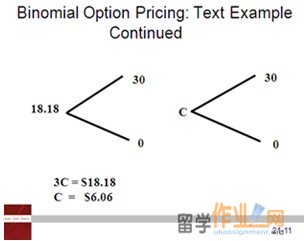

Two-State Option Pricing

Example: Suppose that a stock is selling at $100 now and the price either increases (as denoted by ‘u’ for up) by a factor or 1.20 so it becomes $120, or it falls in value (as denoted by ‘d’ for down) by a factor of 0.90 at time T so the stock is now worth $90.

If a call option is written for the stock with an exercise price of $110, then with the movements in stock price, the payoff from the option will either be $10 or zero.

With this example, the payoff of the call is compared to a portfolio consisting of one share of the stock, and the borrowing of $81.82 at the interest rate of 10%.

If the borrowing of $81.82 is repaid after a year at the interest rate of 10%, it will be the equivalent of $90 at the end of the year.

If the stock price at the end of the year is either $90 or $120, then with the repayment of the loan, with our portfolio consisting of one share of stock and our borrowings, the portfolio payoff is either 0 or $30.

For our portfolio of a share and borrowings, since the initial share cost $100 and we borrowed $81.82, this means we needed to have a cash outlay of $18.18.

|