|

Instructions:说明:

1. There are 2 Sections. Both are compulsory..有2个部分。两者都是强制性的。

2. Section A takes 40% out of 100% and Section B takes 60% out of 100%.A部分占100%的40%,B部分占100%的60%。

3. You must answer 1 question from Section A and 2 questions from Section B, respectively.您必须分别回答A部分中的1个问题和B部分中的2个问题。

4. The total marks available are100 marks..可用的总分为100分。

5. Present Value Table is provided.提供现值表。

6. Use of Calculators is permitted. NO mobiles or other devices are allowed to use.允许使用计算器。不允许使用手机或其他设备。

7. Section A aims to test the understanding and application of theories. Section B focuses on testing the problem solving skills under the context of financial and management accounting.A部分旨在测试理论的理解和应用。 B节侧重于在财务和管理会计的背景下测试解决问题的技能。

8. Section A:Students are expected to use industrial examples to show in-depth understanding and application of the chosen theory as well as critical thinking process. At least, three academic references need be used in the discussion (in-text citation only).A部分旨在测试理论的理解和应用。 B节侧重于在财务和管理会计的背景下测试解决问题的技能。

9. Section B:Students are expected to show the ability to retrieve and make use of the relevant information from the given scenario of a company e.g. financial statement from publicly listed companies, to solve the questions. Students need to show good problem solving skills, in-depth understanding and application of theories, and numeracy in the answers.B部分:希望学生能够检索和利用公司给定场景中的相关信息,例如:来自上市公司的财务报表,解决问题。学生需要表现出良好的解决问题的能力,对理论的深入理解和应用,以及答案中的计算能力。

10. 因为学生要消化、理解所撰写的答案,然后在规定的3小时内闭卷答题,因此复习题答案只要完整、准确即可,字数(words)要考虑闭卷答题书写时间的限制。

Section A – Compulsory (Answer ONE question ONLY) 40%A部分-必修(仅回答一个问题)40%

At least, three academic references (in-text citation only)need be used in the answers per main question e.g. you could provide one academic reference for each sub-question in Question 1.每个主要问题的答案中至少需要使用三个学术参考(仅文本引用),例如,您可以为问题1中的每个子问题提供一个学术参考。

Question 1Purchasing Power Parity问题1购买力平价

a) Critically and analytically discuss the formula of Purchasing Power Parity and the factors that prevent the PPP always holding true in the short run.a)批判性和分析性地讨论购买力平价的公式,以及在短期内阻止购买力平价始终保持不变的因素。

(25分)(25 marks)

购买力平价(Cassel,1918)是一种理论,它规定两国之间的汇率应等于一篮子固定商品和服务的两国价格水平的比率。当一个国家的国内价格水平上升时,该国的汇率必须贬值才能回到购买力平价。因此,购买力平价的比率两国的购买力是决定汇率的基础,汇率的变化是由两国购买力比率的变化引起的。

Purchasing Power Parity(Cassel,1918)is a theory which states thatthe exchange rate between two countries should equal the ratio of the two countries' price level of a fixed basket of goods and services.When a country's domestic price level is increasing, that country's exchange rate must depreciate in order to return to PPP.Therefore, the ratio of the purchasing power of the two countries is the basis for determining the exchange rate, and exchange rate changes are caused by changes in the ratio of the purchasing power of the two countries.

购买力平价的基础是“一个价格定律”(Krugman和Obstfeld,2009年)。“一价定律”涉及市场套利和交易对在两个或两个以上市场交易的相同商品价格的影响。然而,事实并非如此。如(1)运输成本、贸易壁垒和其他交易成本。(2)两国商品和服务的竞争市场十分罕见。(三)一个价格定律只适用于可交易的货物,但许多服务在国家之间不进行交易。(4)一些具体的计算问题,如基期的选择。The basis for PPP is the "law of one price"(Krugman and Obstfeld, 2009). The “law of one price” relates to the impact of market arbitrage and trade on the prices of identical commodities that are exchanged in two or more markets. However, the fact is always not like these. Such as (1) Transportation costs, barriers to trade, and other transaction costsare existing. (2) The competitive markets for the goods and services in both countries are rare. (3) The law of one price only applies to tradeable goods, but manyservices are not traded between countries. (4)Some specific computing problems, like the choice of base period.

PPPdescribes the long run behaviour of exchange rates(Dornbusch, 1976). The change of spot rate is not just determined by the inflation differential between two countries. These factors include: differential of interest rate, differential of income level, the central bank controls, and so on.

References:

Cassel, Gustav (December 1918). "Abnormal Deviations in International Exchanges".28, No. 112 (112). The Economic Journal: 413–415.

Krugman and Obstfeld (2009).International Economics. Pearson Education, Inc.

RudigerDornbusch (1976). "Expectations and Exchange Rate Dynamics".Journal of Political Economy. 84 (6): 1161–1176.

b) Discuss and illustrate the International Fisher Effect with at least one example.

(15 marks)

The Interest Rate Parity theory(Eunet al, 2011) relates exchange rate with risk free interest rates while the Purchasing Power Parity theory relates exchange rate with inflation rates. Putting them together gets: risk free interest rates are related to inflation rates.This brings the International Fisher Effect.IFE theory states that nominal interest rates’differentials between countries reflect anticipated rates of change in the exchange rate of their currencies.

The rationale for the IFE is that a country with a higher interest rate will also tend to have a higherexpected inflation rate (due to the Fisher effect). This increased amount of inflation should cause the currency in the country with the high interest rate to depreciate against a country with lower interest rates (due to the PPP effect).

An example of using the IFE to forecast exchange rate shifts would be: if country A's interest rate is 5% and country B's interest rate is 3%, country B's currency should appreciate roughly 2% compared to country A's currency.

Reference:

Eun, Cheol S.; Resnick, Bruce G. (2011).International Financial Management, 6thEdition. New York, NY: McGraw-Hill/Irwin.

Total Q1: 40 marks

Question 2 Multinational Financial Management

a) Illustrate why businesses might want to internationalise,with two brief business case studies and the potential effects of FOREX changes on the financial situation of MNCs.

(25 marks)

b) Explain and illustrate strategies that MNCs can use to manage transaction exposure under the context of international financial management.

(15 marks)

Total Q2: 40 marks

Section B – Compulsory (Answer TWO questions ONLY) 60%

Question 3

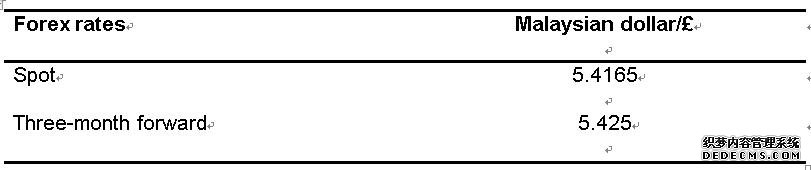

Lozenge plc has taken delivery of 50,000 electronic devices from a Malaysian company. The seller is in a strong bargaining position and has priced the devices in Malaysian dollars at M$12 each. It has granted Lozenge three months’ credit.

The Malaysian interest rate is 3 per cent per quarter.

Lozenge has all its money tied up in its operations but could borrow in sterling at 3 per cent per quarter (three months) if necessary.

A three-month sterling put, Malaysian dollar call currency option with a strike price of M$5.425/£ for M$600,000 is available for a premium of M$15,000.

Required:

a) Conduct a money market and forward hedging strategies, respectively. (Note: explanation of each step in the hedging process, respectively, is essential.)#p#分页标题#e#

(15 marks)

b) Critically evaluate if an option hedge would work given the spot rate M$/£ is going to be either 7 or 4 in three months.

(15 marks)

Total Q3: 30 marks

Question 4

a) A UK importer knows on 1 April that she must pay a foreign seller 26,500 Swiss francs in one month’s time on 1 May. She can arrange a one-month forward exchange contract with her bank on 1 April at a fixed rate of 2.6400 Swiss francs to the £. How much the UK importer has to pay on 1 April to her bank to arrange the forward contract and what is the theory behind your calculation?

26500/2.64=10038£

Base on the pricing of forward contract and no arbitrage rule.

(10 marks)

b) The rate of interest available on a one-year government bond (risk free) in Canada is 5%. A similar bond (risk free) in Australia yields 7%. The current spot rate of exchange is C$1.02/A$. What will be the one-year forward rate if the market obeys the interest rate parity theory?

According to IRP: F= (1+rd)/(1+rf)*S

F= (1+7%)/(1+5%)*(1/1.02)

=0.9987

So one-year forward rateis A$0.9987/C$ or C$1.001/A$

(10 marks)

c) According to b), what would happen if the interest rate parity doesn’t hold and explain?

(10 marks)

According to b),If IRP holds, then one-year forward rateis A$0.9987/C$, arbitrage is not possible.

Following the covered interest arbitragetheory, if the one-year forward rateis less thanA$0.9987/C$enough, arbitrage opportunity exists for investors.Investors can benefit by entering a long position in AUD and simultaneously entering a short position in a forward contract on AUD.

If the one-year forward rateis more thanA$0.9987/C$enough, arbitrage opportunity exists for investors.Investors can benefit by entering a long position in CAD and simultaneously entering a short position in a forward contract on CAD.

Total Q4: 30 marks

Question 5

It is currently April and a UK exporter expects to pay US$1m commission to their US agent at the end of September.

Current spot rate now is £0.63/US$. The quote for September US$ futures is £0.63/US$. The standard size of futures contract is US$70,000.

At the end of September, the UK exporter pays US$1m. The spot rate in September moved to £0.57/US$. The futures rate in September was also £0.57/US$.

Required:

a) Identify the risk that is facing the UK exporter and suggest a strategy to manage the risk.

(3 marks)

b) Illustrate and critically evaluate your chosen strategy.

(20 marks)

c) What could be the alternative strategy if you have access to wider range of financial information e.g. interest rate, financial situation of the company.

(7 marks)

Total Q5: 30 marks

Question 6

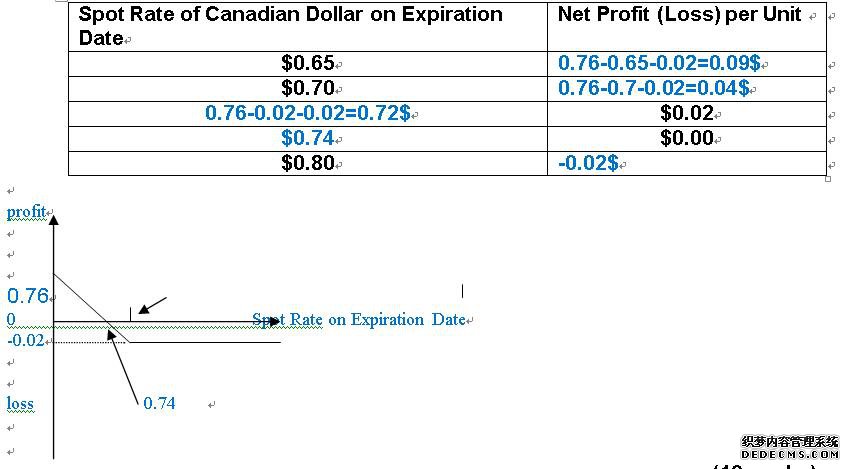

a) Little Liu Co. has purchased Canadian dollar put options for specula¬tive purposes. Each option was purchased for a premium of $.02 per unit, with an exercise price of $.76 per unit. Little Liu Co. will purchase the Canadian dollars just before it exercises the options (if it is feasible to exercise the options). It plans to wait until the expiration date before deciding whether to exercise the options. In the following table, fill in the net profit (or loss) per unit to Little Liu Co. based on the listed possible spot rates of the Canadian dollar on the expiration date. Based on the figures, please graph the profit and loss of the put option position.

(10 marks)

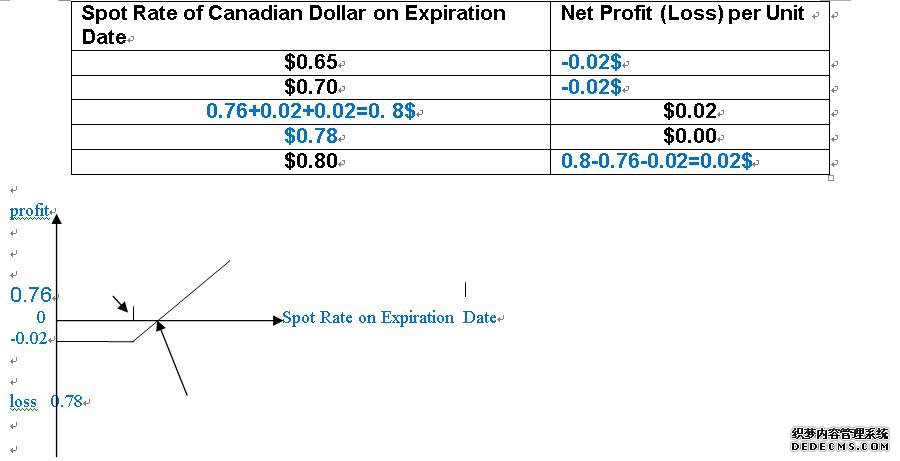

b) How would you change your answer in a) if Little Liu Co. has purchased call options with exactly same characters of the put options?

(5 marks)

c) Critically discuss and compare how the currency financial derivatives i.e. forward, futures and options help MNCs manage the three exposures in international financial management.

(15 marks)

Exchange rates are very volatile. Movement in foreign exchange can affect MNCs in many ways. These risks or exposures may be classified into three different categories:Transactions exposure associates with a transaction that has already been contracted. It is as a result of unexpected changes in foreign exchange rates affecting future cash flows which the MNC has already committed itself to. Usually MNCs enter an international contractual obligation, the payment or receipt of which is expected on a future date, hence any change in the foreign exchange rate during that period will expose the MNC to transaction risks.Translation exposure meansMNC’s financial reporting is affected by exchange rate movements. The consolidation process includes translating foreign assets and liabilities or the financial statements of foreign subsidiaries from foreign to domestic currency. Translation exposure is distinguished from transaction risk as a result of income and losses from various types of risk having different accounting treatments.Economic exposure is the risk not only involves the known cash flows but also future unknown cash flows. It is a comprehensive measure of a company's foreign exchange exposure and therefore sometimes termed as a combination of translation and transaction exposure.

Forward market is the case where the MNC in the forward contract has a legal obligation to buy or sell a given amount of foreign currency at a specific future date which is known as the contract maturity date at a price agreed upon at present.Forward contracts are the most common means of managing transactionsin foreign currencies. The troubleis that sometimes one party is unable to perform on the contract. When thathappens, the hedge disappears, sometimes at great cost to the hedger. Thisdefault risk also means that many companies do not have access to the forwardmarket in sufficient quantity to fully hedge their exchange exposure. Forsuch situations, futures may be more suitable.

Currency futures are similar to foreign exchange forwards inthat they are contracts for delivery of a certain amount of a foreign currencyat some future date and at a known price.But futuresare standardization and are traded in organized exchanges.Furthermore, in a forwardcontract, the transfer of funds takes place at maturity. With futures, cash changes hands every day. This daily cash compensation feature largely eliminatesdefault risk.Thus forwards and futures serve similar purposes, and tend tohave identical rates, but differ in their applicability. Most big companiesuse forwards; futures tend to be used when credit risk may be a problem.

There are a number of circumstances,where it may be desirable to have more flexibility than a forwardprovides.For example, one company’s revenues may be realizedin more than one currency. In such a situation the use of forwardor futures would be inappropriate because of there's no point in hedging somethingyou might not have.Options will be right. Options market which gives MNC the right but not the obligation to buy or sell a specific amount of foreign currency at a specific price, by or on a specific date. It can be useful when a MNC is uncertain about the future receipt or payments of foreign currency.

Total Q6: 30 marks

|

| 网站地图 |