|

1 introduction介绍

欧洲航空公司是英国最大的航空公司,然而,英国决定退出欧洲。在这种政治和经济背景下,公司将失去原有的独特优势,面临经营、财务和其他风险。为了对这些风险进行管理,本文将通过计算对公司的应急预案进行分析和评价,并对公司的外汇风险管理提出建议。

EuroJet is the biggest airline company in the United Kingdom, however, theUnited Kingdomdecides to falls out of Europe. In such a political and economic context, the company will lose its original unique advantage and face with operational, financial, and other risks. In order to manage these risks, the paper will analyze and evaluate the company’s emergency plan by calculation, and offer proposal for its forex ex-change risk management.

2 assumptions假设

如果预测增长率,则使用以下假设进行计算。

1.在项目期间,所有增长率都是恒定的。

2.在表2中,公司对年增长率的最佳估计是由公司完成的,而人事成本可能为5%。

3.关于纳税:假设净现金流量与应纳税所得额相同。

4.公司β系数为0.947。

The calculation using the following assumptions, if the predicted growth rate.

1. All growth rates are constant during the project.

2. In the table 2, the best guess of the annual growth rate is done by the company, besides the personnel cost maybe 5%.

3. About pay taxes: Assume that the net cash flow is same as taxable income.

4. Beta coefficient of the company is 0.947.

3 calculation and analysis计算与分析

3.1 net cash flow 2019-20282019-2028年净现金流量

The Net cash flow (NCF) = cash inflows - cash outflows净现金流(NCF)=现金流入-现金流出

净现金流量是非常重要的,在经营活动、投资活动和融资活动中,相同总现金流量的不同布局意味着不同的财务。一般来说,当经营活动现金流量小于0,投资活动现金流量小于0,融资活动现金流量大于0时,表明公司处于初始阶段,此时公司需要大量现金。经营活动现金流量大于0,投资活动现金流量小于0,融资活动现金流量大于0,说明公司处于高速发展期。当经营活动现金流量大于0,投资活动现金流量大于0,融资活动现金流量小于0时,表明公司产品成熟。当经营活动现金流量小于0,投资活动现金流量大于0,融资活动现金流量小于0时,表明公司处于衰退期。

The net cash flow is very important, different layout of same total amount of cash flow in operate activity, investment activity, and financing activity means different finance. Generally, when the operate activity cash flow is less than 0, the investment activity cash flow is less than 0, the financing activity cash flow is more than 0, it indicates that the company is in initial stage, at this stage the company need a large amount of cash. When the operate activity cash flow is more than 0, the investment activity cash flow is less than 0, the financing activity cash flow is more than 0, it indicates that the company is in high speed development period. When the operate activity cash flow is more than 0, the investment activity cash flow is more than 0, the financing activity cash flow is less than 0, it indicates that the product of compa-ny is mature. When the operate activity cash flow is less than 0, the investment activity cash flow is more than 0, the financing activity cash flow is less than 0, it indicates that the company is in recessionary period.

The calculation is (operation revenue - cash cost) * (1 - tax rate) + depreciation of equipment * tax rate, etc.

2024 refurbishment of aircraft, 12millions of pounds of each aircraft

Constant cost every year: 403 USD

NCF0 initial cash flow: 60 millions of pounds

NCF2019

NCF2020

…

For the case, the operate activity cash flow is more than 0, the investment activity cash flow is more than 0, the financing activity cash flow is less than 0, therefore, the decision is good for the company.

3.2 capital costs

Capital costs are fixed, one-time expenses incurred on the purchase of land, build-ings, construction, and equipment used in the production of goods or in the rendering of services. In other words, it is the total cost needed to bring a project to a commercially operable status. Whether a particular cost is capital or not depend on many factors such as accounting, tax laws, and materiality.

The cost of funds used for financing a business. Cost of capital depends on the mode of financing used – it refers to the cost of equity if the business is financed solely through equity, or to the cost of debt if it is financed solely through debt. Many com-panies use a combination of debt and equity to finance their businesses, and for such companies, their overall cost of capital is derived from a weighted average of all capital sources, widely known as the weighted average cost of capital (WACC). Since the cost of capital represents a hurdle rate that a company must overcome before it can generate value, it is extensively used in the capital budgeting process to determine whether the company should proceed with a project.

The cost of various capital sources varies from company to company, and depends on factors such as its operating history, profitability, credit worthiness, etc. In general, newer enterprises with limited operating histories will have higher costs of capital than established companies with a solid track record, since lenders and investors will demand a higher risk premium for the former.

Every company has to chart out its game plan for financing the business at an early stage. The cost of capital thus becomes a critical factor in deciding which financing track to follow – debt, equity or a combination of the two. Early-stage companies seldom have sizable assets to pledge as collateral for debt financing, so equity financing becomes the default mode of funding for most of them.

In the case of EuroJet:

Capital cost rate of liabilities: issue 320 (m) pound bond, the interest rate is 4%, and expiring in 2026.

Capital cost rate of equity: British financial institutions holds 55% share, 156 (m) in total, equity 78 (m) pound.

According to capital asset pricing model (CAPM), obtain the cost rate=risk-free rate (namely treasury yields) + risk premium = 1.6% + (average yield of all stocks in the market - 1.6%) * 0.947

Market value of liabilities: 320/100*100.51=321.632 (m)

Market value of stock right: 9.68*156=1510.08 (m)

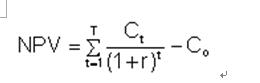

3.3 NPV

Net Present Value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows. NPV is used in capital budgeting to analyze the profitability of a projected investment or project.

A positive net present value indicates that the projected earnings generated by a project or investment (in present dollars) exceeds the anticipated costs (also in present dollars). Generally, an investment with a positive NPV will be a profitable one and one with a negative NPV will result in a net loss. This concept is the basis for the Net Present Value Rule, which dictates that the only investments that should be made are those with positive NPV values.

Calculation for NPV:

PV_ present value

CFt_ cash flow in period t

r_ discount rate

n_ number of time periods

t_ time period

In the case of EuroJet (UK) plc, the NPV>=0, therefore, the protocol that setting up EuroJet (UK) plc is acceptable.

3.4 discounted payback

比较时间长短,做出判断和建议

The discounted payback period is a capital budgeting procedure used to determine the profitability of a project. A discounted payback period gives the number of years it takes to break even from undertaking the initial expenditure, by discounting future cash flows and recognizing the time value of money. The net present value aspect of the discounted payback period does not exist in a payback period in which the gross inflow of future cash flows are not discounted.

The general rule for the calculation is to accept projects that result in a discounted payback period that is less than the targeted period. A company is able to compare its required break-even date to when the project will break even in terms of dis-counted cash flows, to approve or reject the project.

To begin, the cash flow of a project must be estimated and broken down into periods. These cash flows are then reduced by their present value factor to reflect the discounting. With the assumption of a large cash outflow to begin the project, future discounted cash flows are net against the initial outflow. The discounted payback period is calculated when the inflows equal the outflows.

The payback period is the amount of time for a project to break even in cash collec-tions using nominal dollars. Alternatively, the discounted payback period reflects the amount of time necessary to break even in a project based not only on what cash flows occur, but when they occur and the prevailing rate of return in the market. These two calculations, although similar, may not return the same result due to dis-counting of cash flows. For example, projects with higher cash flows toward the end of the project life will experience greater discounting due to compound interest. For this reason, the payback period may return a positive figure, while the discounted payback period returns a negative figure.#p#分页标题#e#

One of the major disadvantages of simple payback period is that it ignores the time value of money. To counter this limitation, an alternative procedure called discounted payback period may be followed, which accounts for time value of money by discounting the cash inflows of the project.

In discounted payback period we have to calculate the present value of each cash inflow taking the start of the first period as zero point. For this purpose the manage-ment has to set a suitable discount rate. The discounted cash inflow for each period is to be calculated using the formula:

Discounted Cash Inflow = Actual Cash Inflow

(1 + i)n

Where,

i is the discount rate;

n is the period to which the cash inflow relates.

Usually the above formula is split into two components which are actual cash inflow and present value factor ( i.e. 1 / ( 1 + i )^n ). Thus discounted cash flow is the prod-uct of actual cash flow and present value factor.

The rest of the procedure is similar to the calculation of simple payback period ex-cept that we have to use the discounted cash flows as calculated above instead of actual cash flows. The cumulative cash flow will be replaced by cumulative dis-counted cash flow.

Discounted Payback Period = A + B

C

Where,

A = Last period with a negative discounted cumulative cash flow;

B = Absolute value of discounted cumulative cash flow at the end of the period A;

C = Discounted cash flow during the period after A.

Note: In the calculation of simple payback period, we could use an alternative formu-la for situations where all the cash inflows were even. That formula won't be applicable here since it is extremely unlikely that discounted cash inflows will be even.

3.5 comparison

两个方法的比较,提出优缺点和各自适应情况

4 forex risk management

The forex exchange risk in the case is embodied in economic risk and accounting risk. In which, the economic risk is that the fluctuations in exchange caused by the United kingdom falling out of the Europe may have influence on the future cash flow net present value of the company, it also may have influence of the profitability and total value (Stockholders' wealth); the accounting risk is that the risk of translation gain or loss occurred when the parent company does combined statements according to different translation rate, it will occur after small company is purchased due to the United Kingdom fails falling out of the Europe.

Regarding to the economic risk, there are two kinds of evasion modes: the first, the finance should be diversified, namely the Financial derivatives hedging is allowed; the second, the operation should be diversified, such as the EuroJetdecides to set a new company, therefore, the change in different exchange rate will be offset between the United Kingdom and the Europe, and the economic risks will be neutralized.

Aiming at accounting risk: The issue of time difference accounts should be considered, it is suggested to shorten the time of currency adjustment. For example, the net capital project from the parent company to the subsidiary corporation, the Early and delayed delivery of the accounts receivable and the accounts payable should be suitably adjusted.

5 conclusion

The project is acceptable

|

| 网站地图 |