|

论文题目:主要是要看两家公司的报表,英文的,然后对比两家公司的现金流表,资产负债表及利润表,找出在structure上的异同点,加以分析说明,以及为什么会造成这样的不同

论文语种:英文

您的研究方向:finace and account

是否有数据处理要求:否

您的国家:英国

您的学校背景:sheffield university 排名15

要求字数:800

论文用途:硕士课程论文 Master Assignment

是否需要盲审(博士或硕士生有这个需要):否

补充要求和说明:Compare the structures of the cash flow statement, the statement of financial position (balance sheet) and the income statement of the two companies. Are they similar in structure or are they different in any material respect? If the structures are different, does either seem to be more useful for making economic decisions than the other and, if so, why? What factors may explain the different structures of these financial statements?引用率不超过14%

1.0 Some specific items to compare the structures of three kinds of statements of the two companies

Generally speaking, no constant or relative stable forms for companies’ financial statements exist whether they are in the same industry or not and how long they will survive in their life cycle (Business statements, 2011).Although http://www.ukassignment.org/dxygessay/ these financial statements may look the same, they actually have differences.Take Japan Tobacco Inc. and Imperial Tobacco Group PLC for example, the former uses the international structure which follows the IAS and IFRS(Alfredson, et al., 2007)and the latter UK structure according to UK GAAP.Hence, specific comparisons are as follows.

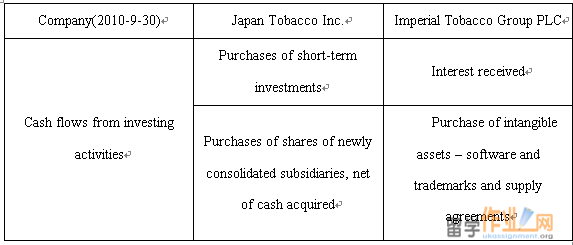

1.1Cash flow statement

To begin with, it’s clearly that no specific items in IMT but a direct “Cash flows fromoperating activities” while JT has an adjustment form EBIT to the last result. Then, as regards to “Cash flows from investing &financing activities”, there is much difference, such as different definition for the same item (“Interest received” in IMT but “Purchases of short-term investments” in JT) and different specific items which can be seem from table1 (Knight, 1998). At last, there is an enumeration of cash changes from “Exclusion ofSubsidiaries from Consolidation in JT”. That’s all for the different business in between.

Of course, there is certain of similarity. For example, the basic thoughtsof the cash flow statement are the same as they all begin from threekinds of activities, then find the respective net cash flow and then obtain the last result of Cash and cash equivalents at end of year.

1.2Balance sheet

Of course, difference in balance sheet is no surprise. First and foremost, they use different column methods: IMT “Assets-Liability=Equity” and JT“Assets=Liability-Equity”because they mainly adapt different market investors’ habits in their own country(Dichev, 2008). Other details still exist; for instance, IMT begins with non-current assets then current assets while JT is from current assets to investments and other assets. Obviously, the INT structure adopted by JT will rank its accounting elements in accords with its liquidity while the UN not(Haller, 2002). However, the specific classification is similar, such as the Inventories in Current assetssequence and Intangible assets in Non-current assetssequence.

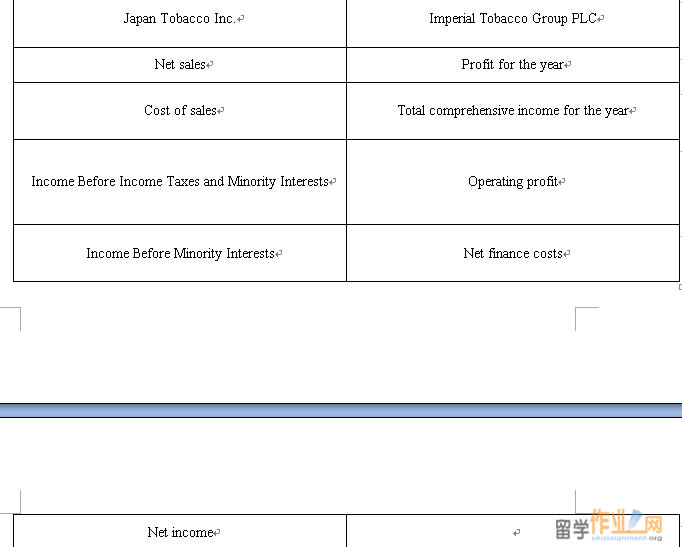

1.3Income statement

In terms of income statement, different column methods are adopted: IMT single-step style and JT multi-step style which can also be seen as the UK GAAPand IAS style. Hence, the former is from profit to profit while the latter from operating income to EBIT to net income (Karreman, 2008).The specific calculation process is as follows. Apparently, the INT structure is more detailed in the expressionof statement than the UK structure.

2.0 Reasons to explain which structure is more useful for making economic decisionsand factors accounting for the difference of the structures

As regard to the question that which structure style is better, the author thinks, there is still a large space of improvement for the UK structure. Although the IAS and IFRS are often criticized for its complexity, the UK GAAP actually has a lot of disadvantages. Drew by authoritative agency, IAS aims to make up a globally universal framework and principle to accord with international needs (Langerand Lev, 1993). Specifically speaking, firstly,international investors hope to be able to understand and use foreign statements easily.Then, for an international company, it is easier to accept international management,prepare consolidated report and arrange its accounting personnelWorldwide. Following this, the European Union has required all its members to prepare consolidated statements according to the IFRSsince 2005 (Leuz , 2003). Finally, the listed company may bypass the many obstacles to finance in other countries if abiding by IAS.Therefore, the IAS structure is more useful for making economic decisions.

The factors accounting for the difference of the structurescan be seen from macro level and micro level.On the Macro Level,the emergence and development of accounting principles are different.To be specific, one’s political and social environment, economic development, legal environment and tax system willexpand the gap(Wilkinson,et al., 2000).Those factors can be summarized as the region factors. Of course, these factors lead to the definitions of assets, liabilities, equities, income and expenses, the different use of standard confirm as measurement basis and the scope and the content of the financial statements. On the other, other factors that bring about the changes are its development stage, life cycle, economy of scale, the objectives of the company, the management investing decision and etc.For example, as a multinational company, there will be a reasonable guess that its balance sheet will be an“Assets-Liability=Equity” one according to the IAS.From the analysis above, region factors can be dominant to decide the statements’ structures and the others play affiliate roles.

3.0 Reference

Alfredson, K., Leo, K., Picker, R., Pacter, P., Radford, J.& Wise. V., 2007. Applyinginternational financial reporting standards. Queensland Australia: John Wiley & SonsAustralia Ltd.

Business statements, 2011.Financial statements.[online]Available at: [Accessed 10December 2011].

Dichev, I. D., 2008. On the balance sheet-based model of financial reporting. AccountingHorizons,vol.22,pp.453-470.

Haller Axel, 2002.Financial accounting developments in the European Union: Past events and future prospects.European Accounting Review, vol. 11, pp. 153–190.

KarremanB., 2008. Financial geographies and emerging markets in Europe.Journal of Economic and Social Geography, vol. 99, pp. 1–18.

KnightM.D., 1998.Developing countries and the globalization of financial markets, World Development, vol.26, pp.1185–1200.

Langer, R. and LevB., 1993.The FASB's Policy of Extended Adoption for New Standards: AnExamination of FAS No. 87.The Accounting Review, 68(3),pp. 515-533.

Leuz, C., 2003. IAS Versus U.S. GAAP: Information Asymmetry Based Evidence http://www.ukassignment.org/dxygessay/ from Germany'sNew Market.Journal of Accounting Research, 41(3),pp.445-472.

Wilkinson, J.W.& Cerullo, M.J.& Raval, V.& Wong-On-Wing, B., 2000.Accounting informationsystems: Essential concepts and applications. New Jersey: John Wiley and Sons, Inc.

|