|

ABF305 Investment Management

Lecture 3

ABF305投资管理

第3讲

Housekeeping:

内务处理:

How the workshops will be run:

研讨会将如何运行:

Each workshop session will begin with selected groups presenting their answers for the group assignments. You take on the role of the teacher.

每个研讨会议将开始与所选组的组分配提出自己的答案。你担任老师的角色。

Thereafter, in your groups you will tackle unseen questions.

此后,在你的群体,你会对付看不见的问题。

A review of last week:

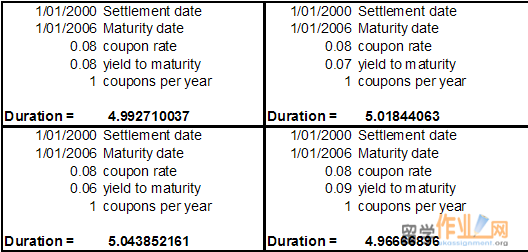

The five rules of duration demonstrate how sensitive a bond price is to changes in the interest rate, coupon, and bond maturity.

The resultant gains and losses make fixed-income investments like bonds risky even if the coupon and principal payments are guaranteed.

Since duration allows us to see the price sensitivity for a bond, this ability allows us to find bonds whose prices move in the opposite direction to ours.

That way we can neutralize or in more technical terms, immunize the risk for our bond portfolio.

The textbook definition for immunization is ‘A strategy that matches durations of assets and liabilities so as to make net worth unaffected by interest rate movements’. (Bodie, Kane and Marcus, ‘Investments’, 8th Edition)

免疫的教科书的定义是“持续时间相匹配的资产及负债,从而使净值不受利率变动”的策略。 (博迪,凯恩和马库斯,“投资”,第8版)

Another textbook definition for immunization is ‘A bond portfolio management technique of matching modified duration to the investment horizon of the portfolio to eliminate interest rate risk’. (Reilly and Brown, ‘Investment Analysis and Portfolio Management’, 8th Edition).

另一个教科书免疫的定义是'A的债券投资组合管理技术,修正久期匹配的投资期限组合,以消除利率风险'。 (Reilly和布朗,投资分析和投资组合管理“,第8版)。

Let us see what this means with an example:

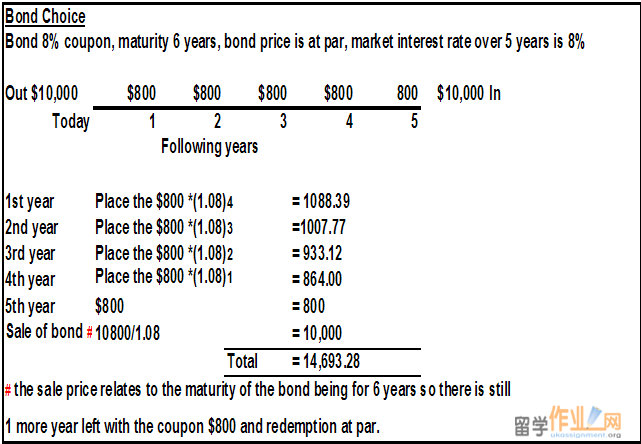

We are insurance investment managers and we have issued a guaranteed investment contract whose terms are as follows:

Principal of $10,000. Pays 8% interest. 5 year maturity. Interest plus principal paid on maturity. So our obligation is $10,000 * (1.08)5 = $14,693.28 at the end of 5 years.

To fund this obligation you could:

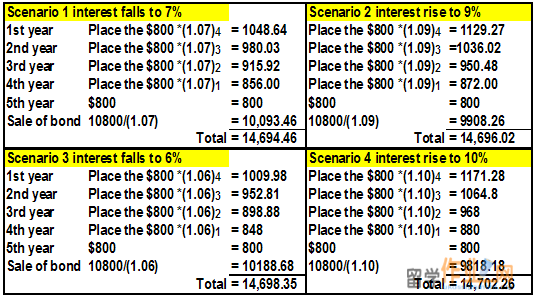

With a change in interest rates, we observe a mismatch in cash flows:

Another way to demonstrate this mismatch is through the duration.

As such, duration may be employed in portfolio management to reduce the interest rate risk of a bond portfolio by matching the modified duration of the portfolio with its investment horizon.

Problem!

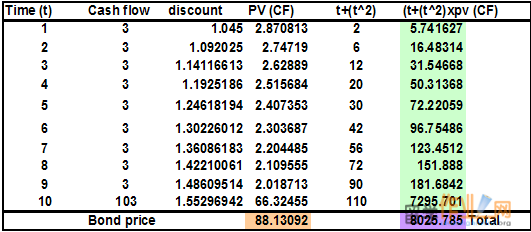

Duration is inaccurate for larger changes in interest rates because it is a linear relationship. It does not account for the fact that the price-yield relationship for a bond is not linear but it is in fact curved.

时间是利率的变化较大,不准确的,因为它是一个线性的关系。它没有考虑价格收率一个键的关系的事实,不是线性的,但它实际上是弯曲的。

To address this issue, the formula below for the percentage price changing using duration is adjusted for by the curvature which represents the bonds’ price-yield relationship.

To address this issue, the formula below for the percentage price changing using duration is adjusted for by the curvature (convexity) which represents the bonds’ price-yield relationship.

Convexity is calculated as:

Thus far, the focus has been on passive investment management.

What about active investment management?

关于主动投资管理的是什么?

The textbook definition for active management is, it ‘attempts to achieve portfolio returns more than commensurate with risk, either by forecasting broad market trends or by identifying particular mispriced sectors of a market or securities in a market’.

(Bodie, Kane and Marcus, ‘Investments’ 8th Edition).

教科书定义为主动管理,努力实现投资组合的回报与风险相称,无论是广阔的市场发展趋势预测或识别特定市场或证券在市场错误定价的行业。

(博迪,凯恩和马库斯,“投资”第八版)。

For bonds, this can be achieved by:

A general viewpoint for which you forecast interest rate movements. You may forecast an interest rate to fall or rise for example in the future. Any changes will affect the entire spectrum of the fixed income market.

The second source is from a specific viewpoint whereby you identify a specific mispriced asset.

Active bond management can therefore be decomposed into broadly speaking, either:

(1) Interest rate forecasting techniques; and;

(2) Intermarket spread analysis.

With respect to active management:

5 strategies available are:

(1) Interest rate anticipation;

(2) Valuation analysis;

(3) Credit analysis;

(4) Yield spread analysis; and

(5) Bond swaps.

Within bond swaps, there are 4 commonly used:

They were identified by Homer and Leibowitz (1972) as:

A substitution swap

An intermarket spread swap

A rate anticipation swap

A pure yield pickup swap.

|