|

Examples of WACC from Arnold Ch.19

来自阿诺德Ch.19加权平均资本成本的例子

Illustration of WACC

加权平均资本成本的说明

•A firm invested £100,000 in a project that produced a net cash flow per year of £10,000 to infinity

一个公司投资100,000英镑到无穷大项目,产生了每年10,000英镑的现金流量净额

•Debt holders require £4,000 per annum (8 per cent)

债务持有人需要每年4,000英镑(8%)

•Leaves £6,000 for equity holders – an annual return of 12 per cent on the £50,000 they provided

为权益持有人留下6,000英镑 - 50,000英镑,他们提供的年回报率为12%

•An overall return of 10 per cent (the WACC) provides an 8 per cent return on the capital supplied by lenders and 12 per cent on the capital supplied by shareholders

整体10%的回报率(加权平均资本成本)提供了8%的资本回报由贷方和12%,提供由股东提供的资本

•A return of £11,000 (i.e. 11 per cent) is generated

返回11000英镑(即11%)产生

•Debt holders receive £4,000

债务持有人收到4000英镑

•Equity holders get a 14 per cent return: £7,000 on their £50,000

权益持有人获得了14%的回报率:£7,000其50000英镑

Lowering the WACC and increasing shareholder returns

降低加权平均资本成本和增加股东回报

http://www.ukassignment.org/dxygassignment/

•If the company is expected to produce £100 million cash flow per year (to infinity), and its WACC is 10 per cent, its total corporate value (‘enterprise’ value that is, the value of the debt and equity) is:

£100 million / 0.10 = £1,000 million

•Firm set up with 70 per cent debt

WACC = kEWE + kDWD

WACC = (12 × 0.3) + (8 × 0.7) = 9.2%

Firm value = £100 million /0.092 = £1,086.96 million

Lowering the WACC?

降低加权平均资本成本

•If a rise in kE exactly offset the benefit from the increase in the debt proportion; leaving the WACC constant

WACC = kE WE + kD WD

WACC = (14.67 × 0.3) + (8 × 0.7) = 10%

•Modigliani and Miller left out at least two important factors:

–Tax

–Financial distress

The benefit of tax

税收的好处

Lowering the WACC due to the tax shield

由于税盾效应降低加权平均资本成本,

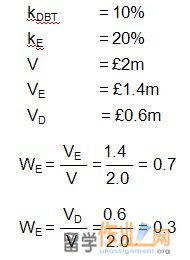

kDBT = Cost of debt before tax benefit = 8%

kDAT = Cost of debt after tax benefit = 8 (1 – T) = 8 (1 – 0.30) = 5.6%

•If we assume a 50 : 50 capital structure the WACC is:

WACC = kE WE + kDAT WD

WACC = (12 × 0.5) + (5.6 × 0.5) = 8.8%

•Investment project cash flows discounted at this lower rate will have a higher present value than if discounted at 10 per cent

•This extra value flows to shareholders

WACC with tax and financial distress

加权平均资本成本税收和财务困境

•The required return on equity rises from 12 per cent to 13 per cent when the proportion of the debt in the capital structure rises to 65 per cent

所需的股本回报率上升,从12%到13%,债务资本结构的比例上升到65%

•The effective rate of return payable on debt is 5.6 per cent after the tax shield benefit

税盾利益后有效应付债务回报率5.6%

•The WACC falls and the value available for shareholders rises

加权平均资本成本下降和值可供股东上升

WACC = kE WE + kDAT WD

WACC = (13 × 0.35) + (5.6 × 0.65) = 8.19%

•Assume that 65 per cent gearing is the optimum debt/equity ratio

假设65%的资产负债是最佳的债务/权益比率

•If we go to 80 per cent debt we find this reduces shareholder wealth

如果我们去到80%的债务,我们觉得这是减少股东财富

WACC = kE WE + kDAT WD

WACC = (30 × 0. 2) + (7 × 0.8) = 11.6%

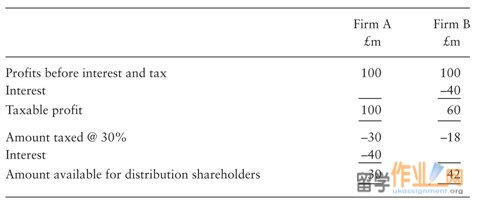

Worked example: Poise plc

处理过的例子:Poise有限公司

Poise: WACC calculation

Poise: 加权平均资本成本的计算

kDAT = kDBT (1 – T)

kDAT = 10 (1 – 0.30) = 7%

WACC = kE WE + kDAT WD = 20% × 0.7 + 7% × 0.3 = 16.1%

•An investment of £1m at Time 0 produces after tax annual cash flows before interest payments of £161,000 as a perpetuity a 16.1 per cent rate of return

投资时间0时产生100万英镑的年度税后现金流量作为永久161000英镑付息前16.1%的回报率

•The net cost of satisfying the debt holders after the tax shield benefit is £21,000

税盾利益满足后的债务持有人的净成本是21000英镑

•Shareholders receive £140,000 per year, a 20 per cent return on the £700,000 they supplied

股东获得£140,000每年20%的回报,他们提供700000英镑

•If th e project produces £100,000 the debt holders receive £21,000, leaving only £79,000 for the shareholders a mere 11.3 per cent return

如果项目产生100000英镑,债务持有人获得£21,000点,留下只有79,000英镑的股东仅有11.3%的回报率

|